On May first, the Commission released a landmark Report and Order replacing decades-old energy caps with a performance-based spectrum sharing framework. The ruling is designed to sharpen competition between satellite, cable, and terrestrial wireless providers. And then, on May twelfth, the F-C-C issued a separate approval for SpaceX to acquire approximately 65 megahertz of mid-band spectrum from EchoStar Corporation -- in a 17-billion-dollar transaction.

That spectrum -- covering AWS-4, AWS H-Block, and unpaired AWS-3 licenses -- is the foundational layer SpaceX needs for its next-generation Direct-to-Device network. Commercial D-2-D services could begin as early as late 2026 for initial messaging and emergency alerts, with full constellation buildout extending through the next several years.

Layer on top of that what the F-C-C had already done in April for AST SpaceMobile. The Commission granted AST commercial authorization to deploy a constellation of 248 satellites providing supplemental coverage from space -- using low-band 700 and 800 megahertz spectrum in coordination with Verizon, AT&T, and FirstNet. Half the constellation -- 124 satellites -- must be in orbit by August of 2030.

And then this week, the story got even bigger. AT&T, T-Mobile, and Verizon announced plans for a joint venture to expand satellite-based direct-to-device connectivity across the United States -- specifically targeting unserved and underserved areas. The joint venture would pool spectrum, create common technical standards, and build what the carriers are calling a technology-neutral platform that any qualified satellite operator can plug into.

The three carriers aren’t just customers here. They are becoming the infrastructure layer that determines which satellite operators succeed at commercial scale. For investors and supply chain managers watching the D-2-D market -- the regulatory and commercial framework just got a lot more real.

-0-

NASA has proposed a CLPS 2-point-0 procurement -- a competitive follow-on to its Commercial Lunar Payload Services program -- and the agency intends to launch monthly uncrewed missions to the Moon beginning next year. To support that cadence, NASA moved to raise the CLPS contract ceiling to 4-point-2 billion dollars. (Paywall)

The most recent award went to Intuitive Machines -- a 180-point-4-million-dollar contract to deliver seven science and technology payloads to the Lunar South Pole region. That’s Intuitive Machines’ fifth CLPS task order. For context -- this is the company that successfully landed the first commercial spacecraft on the Moon in 2024.

On the private side, Lunar Outpost just closed a 30-million-dollar Series B -- oversubscribed -- led by Industrious Ventures. The company now has eight fully contracted lunar and cislunar missions on its manifest before 2030, more than any other commercial surface-mobility provider. Revenue has doubled each year for four consecutive years.

The White House is leaning in as well. The Trump administration’s commercial-first architecture is explicitly targeting lunar surface presence by 2028, framing satellite connectivity and lunar logistics as critical national infrastructure.

The question worth tracking is not whether the lunar market is real. It is. The question is whether the supply chain serving it can scale fast enough. Component lead times, launch cadence, and ground infrastructure are the binding constraints -- and those are exactly the kinds of gaps that create near-term opportunities for suppliers who move early.

-0-

The GEO-to-LEO transition has stopped being a debate. It is now an operating reality -- and the numbers from early 2026 earnings make that clear. (Paywall)

Eutelsat Group’s early-2026 results showed LEO revenues surging nearly 60 percent year-over-year, while GEO revenues declined 4-point-5 percent. For the first time, the growth curve of the new business visibly outpaced the decline of the old one. Eutelsat followed that with a contract with Airbus valued at between $2.34 and $2.57 billion dollars for 340 additional LEO satellites -- backed by a $1.75 billion capital increase supported by the French and British governments. Those governments aren’t just writing checks. They’re treating satellite connectivity as critical national infrastructure, and they want sovereign capacity that Starlink cannot provide.

Telesat Canada tells a different version of the same story -- and a more turbulent one. The company faces a 1-point-7-billion-dollar debt maturity wall in December 2026, and creditor litigation alleging it moved its LEO constellation assets beyond the reach of GEO-linked lenders. Telesat has dismissed the suits. Its prime contractor MDA Space is completing a high-volume manufacturing facility in Quebec aimed at a full launch cadence of 156 Lightspeed satellites by end of 2027.

SES and Intelsat merged for 3-point-1 billion dollars, creating a combined fleet of 120 satellites and projecting free cash flow above $1.17 billion annually by 2027 and 2028. The merged entity’s highest-growth segments now account for roughly 60 percent of combined revenue -- including medium-Earth-orbit capacity serving NATO and defense clients.

The through-line: the concept of multi-orbit has moved from conference keynote buzzword to core operating model. Companies that couldn’t afford to make this transition aren’t around to talk about it anymore. The ones still standing -- Eutelsat, SES-Intelsat, Viasat -- are building hybrid architectures that neither orbit can serve alone. The hard part isn’t the boardroom decision. It’s the engineering: creating a system that will enable seamless handovers between disparate orbits for a passenger mid-flight or a naval vessel mid-maneuver. None of the major operators have demonstrated that at commercial scale. That is the milestone the industry’s credibility depends on.

-0-

SpaceX has confidentially filed with the Securities and Exchange Commission and is targeting a late June initial public offering. The numbers being discussed are unlike anything the public markets have ever processed. (Paywall)

The most recent reporting puts the target valuation between 1-point-5 and 1-point-75 trillion dollars, with a fundraising goal between 50 and 75 billion dollars. Either figure would shatter the record set by Saudi Aramco’s 29-billion-dollar offering in 2019. At 1-point-75 trillion, SpaceX would enter the public market in the same bracket as Alphabet and Amazon. Prediction markets as of this week placed the probability of a June 30th listing at around 72 percent.

SpaceX is essentially three businesses operating in parallel: Starlink, which generates the bulk of current revenue growth; the launch business, which has no close competitor on cost or cadence; and a nascent space infrastructure and A-I platform play that Elon Musk has described as Space A-I Data Centers.

For space commerce investors and analysts -- the I-P-O matters beyond the price. A public SpaceX will file quarterly reports. For the first time, the market will have standardized financial visibility into the company that now controls a dominant share of global launch capacity, the world’s largest satellite constellation, and the regulatory approvals shaping the entire direct-to-device market. The information environment around space commerce changes materially the day that S-1 becomes public.

-0-

A new analysis published this week by the Journal of Space Commerce maps a supply chain constraint that most constellation programs haven’t fully priced in: space-grade solar cells. (Paywall)

Novaspace’s latest market report projects 16-thousand-900 small satellites launching between 2026 and 2035 -- roughly 1,400 pounds of hardware delivered to orbit every single day. But that headline number actually understates the pressure on the solar cell supply chain. In April, Space Systems Command awarded 20 Other Transaction Authority contracts worth up to 3-point-2 billion dollars to 12 companies prototyping orbital Space-Based Interceptors for the Golden Dome missile defense architecture -- including Anduril, Lockheed Martin, Northrop Grumman, SpaceX, and Raytheon. Each of those prototype satellites carries power requirements that must be met by space-qualified solar cells from the same supplier base already serving the commercial constellation market. None of that demand appears in the commercial procurement pipelines.

The qualified supplier base for space-grade gallium arsenide solar cells comes down to two dominant players: Spectrolab -- a Boeing subsidiary in California -- and AZUR SPACE Solar Power, based in Germany. AZUR has been expanding aggressively -- up 35 percent in 2024, 30 percent in 2025, another 25 percent expansion announced in February for second-half 2026. Over three years, that’s roughly a 118 percent capacity increase.

The problem is the baseline those percentages are measured against. It was already considered a bottleneck before the 2026 demand acceleration. And the binding constraint in that particular solar cell supply chain isn’t cell assembly -- it’s germanium wafers, the semiconductor substrate on which every triple-junction cell is built. The global germanium wafer market for space solar applications had a total value of approximately 125 million dollars in 2024. That is a small market to underpin 16-thousand-900 satellites, a proliferated interceptor constellation, and multiple sovereign programs.

That germanium market is dominated by two players: Umicore, a Belgian materials company -- and China Germanium, a state-linked Chinese enterprise. China accounts for roughly 60 percent of global refined germanium output. In a scenario where export controls tighten or U-S-China trade tensions escalate further, a germanium supply disruption would propagate through the entire Ga-As cell production base.

The downstream signal is already visible. Satellite integrators and mission designers have reported significant delays in solar cell procurement, with lead times lengthening and costs rising. For small satellite programs on fixed-price contracts, this is an active schedule and margin threat. For supply chain leaders -- the window to lock in 2027 and 2028 production slots is closing faster than most forward procurement schedules assume.

-0-

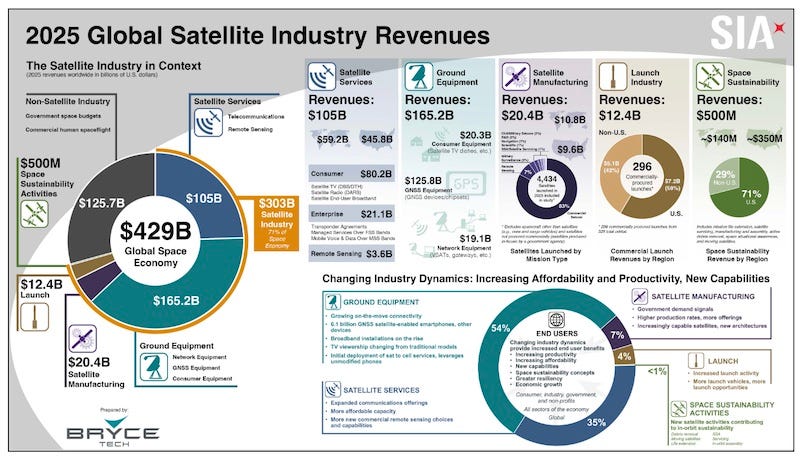

The Satellite Industry Association has released its 29th Annual State of the Satellite Industry Report, and Ex Terra Media sat down with SIA President Tom Stroup to discuss the findings.

The commercial satellite industry wrapped up 2025 with records across the board -- more launches, more satellites, and more subscribers than ever before. Stroup says two forces are behind the surge.

“I think it’s a combination of both demand and the ability to be able to manufacture and launch much more cost effectively than in the past. The vast majority of those satellites that were launched last year were for communications purposes. We’ve seen that access to broadband is considered essential across the globe,” Stroup said. “The demand is there for more and more connectivity and it doesn’t matter whether it’s consumers at home or whether it’s on board airplanes or maritime vessels. There’s an expectation that people are going to have access to the broadband service no matter where they are.”

The price drop is just as significant as the technology leap. Stroup says satellite broadband is now competing directly with cable and fiber on cost.

“The service starts at about fifty dollars a month. The cost of terminals is continuing to decrease. I think that the typical cost now is fifty dollars or less. So the ability to be able to manufacture and launch them and be cost effective is really the other major aspect of it.”

Satellite broadband subscribers topped 10 million in 2025 -- a 62 percent jump in a single year. Stroup calls it a milestone -- but says the industry is just getting started.

“I think it’s a very important milestone. But in some ways I’m just going to say it’s another number because we’re going to see 15 million, 20 million. The number is just going to continue to increase as more and more people who have not had access to broadband services are able to be served because of the ubiquitous coverage that the industry provides,” Stroup said.

That growth is already rattling the competition on the ground. According to Stroup, those cable companies, those fiber companies that are in areas where they’ve been operating as monopolies are going to have to deal with competition from satellite companies that are providing very high speeds, high capacity, at very competitive prices. Meanwhile, manufacturing the satellites driving that growth is a massive undertaking -- and not without bottlenecks. Stroup says the supply chain is under strain.

“We end up having to compete for chips as an example with other technology industries. But ours have the additional need of being radiation resistant,” Stroup said. “And there are other components -- just nozzles would be one example, the fuel containers that are used for launch -- those are still relatively small numbers. So those are some of the areas where we’re encountering supply chain issues.”

One of the industry’s most-watched emerging sectors is Direct-to-Device -- the ability to connect a standard smartphone directly to a satellite. Stroup says it has moved from science fiction to shop floor. “The systems are being deployed. It’s just been a fascinating transition because we’ve gone from 10 years ago, people saying there’s no way you could make this work, to basically most satellite operators having a strategy in place and feeling that they need to have either partnerships or deployment plans,” he said. “We’ve already seen lives saved as a result of some of the emergency capabilities.”

And mainstream consumers are already hearing about it.

“Last year for the first time we saw mobile companies advertising their satellite capability -- whether it was at the Super Bowl or award ceremonies,” he continued. “It was the mobile companies who were making the announcements of that capability, because they see it as very important to their ability to compete with other mobile companies.”

On Capitol Hill, Stroup says SIA’s top priority is securing U-S influence at the next World Radiocommunication Conference -- known as WRC-27 -- where global spectrum policy will be set. “Over 80 percent of the issues at WRC-27 are going to be related to satellites. I would say that congressional support for the U.S. naming the head of the delegation and then making sure that they’re encouraging the administration to move forward with positions that are supportive of the industry.”

Stroup also sees China as the defining competitive threat -- and draws a cautionary parallel to the wireless infrastructure wars of the last decade. “One of the best examples would be Huawei. What they did with respect to infrastructure, especially for the wireless industry -- they were a very effective competitor, offering subsidized equipment that had a very negative impact on other manufacturers, both in the United States and in Europe,” he said. “We’re quite positive that Chinese companies that are going to be providing satellite-based services are going to do so at subsidized rates. So to the extent that they’re offering subsidized services in developing areas of the world, there’s a great risk to the United States.

“The good news is we’ve got a lot of innovation capital coming into the industry, supportive government. But that needs to continue to make sure that we maintain our leadership position,” Stroup said

The full State of the Satellite Industry Report is available through the Satellite Industry Association’s website.

-0-

Worth a Second Look

Five Skills Every Space Communicator Needs — And Where the Gaps Are (Paywall)

The NASA Station Award That Cannot Slip (Paywall)

Acquisition Would Create Integrated Commercial Lunar Communications Network

Positioning, Without the Satellite

When (And Why) NASA Partners Instead of Buys