The European Union is pressing ahead with its landmark EU Space Act — even as the regulation faces mounting legal questions from its own advisers and a sharp rebuke from the United States government.

The Council of the EU circulated a Presidency compromise text this spring, with a key negotiating session scheduled for April 21st. But the road to final agreement is getting more complicated by the week.

Here’s the backdrop: the EU Space Act is designed to replace a patchwork of national licensing regimes. Thirteen EU member states have enacted their own space laws — often with conflicting standards. The act would create one unified framework covering safety, resilience and environmental sustainability, and it would establish a new certification system called the EU Space Authorization — or EUSA — for satellite operators, launch providers and related space services companies.

But the Council’s own Legal Service raised red flags in a January opinion, concluding that while the act’s core provisions are legally sound, its reach into the downstream data economy is questionable. Specifically, the legal advisers warned that requiring so-called “primary providers” — satellite communications and Earth observation companies that act as data intermediaries — to verify that all their data comes from EUSA-compliant satellites may be disproportionate. The opinion stated, quote, “In the absence of adequate evidence and explanation, it is questionable whether this approach is proportionate and remains within the limits of the proposed legal basis,” end quote.

And that’s not the only pressure point.

The United States government formally objected to the draft regulation in November 2025, with the State Department submitting comments calling several provisions, quote, “unacceptable regulatory burdens” on American companies doing business in Europe.

The Office of Space Commerce coordinated the U.S. response — working with more than 70 American companies and multiple trade associations. Washington’s position: the EU Space Act contradicts commitments made under a U.S.-EU framework agreement signed in August 2025 aimed at reducing non-tariff trade barriers.

The U.S. is asking Brussels to align the act with internationally agreed guidelines rather than writing new unilateral standards, to create clear equivalency pathways for non-EU operators, and to publish key implementation details directly in the regulation text — rather than leaving them to be filled in later by Commission officials.

The anti-circumvention provisions targeting so-called “gatekeeper” entities in the data market remain the most contested elements. Those provisions drew both the legal proportionality concerns from the EU’s own lawyers and the trade objections from Washington. The April 21st working party session will be a critical test of whether negotiators can resolve those issues — or whether this landmark regulation hits another wall.

All delegations currently have scrutiny reservations on the text. In plain language: nobody has signed off yet.

-0-

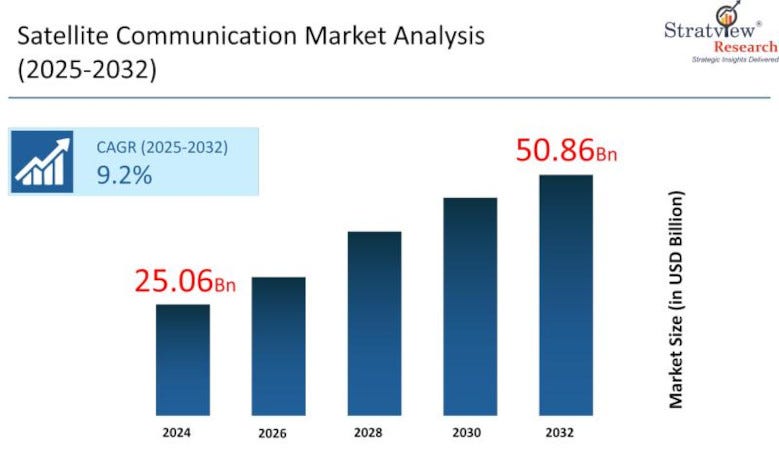

A new report from Stratview Research projects the global satellite communications market will reach $50.86 billion by 2032, growing at a compound annual rate of 9.2 percent.

The headline driver: rising demand for connectivity in remote and underserved areas. Satellite systems are filling a gap that ground-based infrastructure simply cannot reach — and that gap, by the numbers, is enormous.

A few details worth noting from the report:

Broadcast services are expected to hold the largest market share across the forecast period. The demand for high-quality, uninterrupted digital content delivery is a key factor, and satellite broadcasting has a reliable infrastructure edge over terrestrial networks in wide-area coverage.

On the consumer side, Direct-to-Home — or DTH — service is projected to remain the dominant application segment. That’s driven by strong subscriber demand for personalized, high-quality content delivered directly to households, including in markets where traditional cable or fiber infrastructure doesn’t reach.

The fastest-growing end-user category is the enterprise segment. Industries like mining, oil and gas, aviation, telecom and defense are all leaning harder on satellite communications for reliable connectivity in environments where no terrestrial option exists.

And geographically, North America is expected to be both the leading and fastest-growing region over the forecast period — driven by government investment, mature technology capabilities and the presence of major industry players. The integration of 5G, artificial intelligence and cloud-based satellite systems is accelerating real-time connectivity and expanding application areas. Defense communication and secure data transmission are also strengthening demand.

So — just shy of 51 billion dollars by 2032, growing at better than nine percent a year. Those are the numbers shaping where investment, competition and regulatory attention in this space are headed.

-0-

Rocket Lab’s acquisition of German laser communications company Mynaric (mun-AHR-ic) has cleared a significant regulatory hurdle — and it brings a critical satellite technology in-house for one of the industry’s most aggressive vertical integrators.

Germany’s Federal Ministry for Economic Affairs and Energy has reviewed and approved the deal. The transaction is not yet closed, but regulatory approval in Germany is a major milestone.

So why does this matter?

Laser communications — also called optical inter-satellite links — represent a fundamental shift in how satellite constellations talk to each other and relay data to the ground. Compared to traditional radio frequency systems, laser comm offers higher data rates, better security, greater scalability and more efficient use of spectrum. The problem has been supply. For constellation operators trying to build at scale, laser comm terminals have been a persistent bottleneck — hard to source in volume, expensive, and often delayed.

Rocket Lab CEO Sir Peter Beck put it plainly. Quote: “Laser communications are a critical enabler for the constellations of today and tomorrow, and Rocket Lab is going to make them available at scale.” End quote.

The acquisition follows a pattern Rocket Lab has executed before. The company has a track record of identifying satellite subsystems that are only available in small quantities and at high prices — and then scaling production to serve the broader market. From solar panels to reaction wheels and star trackers — Rocket Lab has done this across multiple components. The pitch with Mynaric is the same playbook applied to optical terminals.

There’s already an existing relationship here. Mynaric is a subcontractor to Rocket Lab, providing CONDOR Mk3 optical terminals for Rocket Lab’s 1.3-billion-dollar prime contracts with the Space Development Agency — covering 36 satellites across the Transport Layer-Beta Tranche 2 and Tracking Layer Tranche 3 programs. Mynaric also supplies other SDA contracts, and the two companies share a significant customer overlap across commercial constellation operators and defense agencies.

After closing, Mynaric will remain headquartered in Munich, Germany — establishing Rocket Lab’s first European footprint and expanding its ability to serve German and broader European space programs.

Planet Labs has announced what it’s calling a landmark technical achievement — and it’s a genuine one. The company successfully deployed and ran artificial intelligence object detection directly onboard its Pelican-4 satellite. No downlink. No waiting. The analysis happened in orbit.

Here’s the specifics: On March 25th, Planet’s Pelican-4 satellite was flying approximately 500 kilometers — about 310 miles — over Alice Springs, Australia. The satellite captured an image of an airport and then used its onboard NVIDIA Jetson Orin module to run an AI model that detected airplanes in the image — in moments.

Planet describes this as one of the first times an Earth imaging satellite has moved beyond simple data capture to actual onboard AI inference. The company calls this vision “Planetary Intelligence.”

Why does it matter? Because the traditional model in satellite Earth observation has been: capture an image, downlink it to a ground station, process it on the ground, then get the result to the customer. That pipeline can take hours. Moving AI to the edge — to the satellite itself — collapses that window to minutes.

Planet CEO Will Marshall added that the company is, quote, “moving AI from the internet into the physical realm — effectively connecting the ‘eyes’ of our satellites with an onboard ‘brain’ to create a nervous system for the planet.”

The practical applications here are immediate: disaster response, security monitoring, logistics — any scenario where minutes matter. The end-to-end process, from image capture to AI analysis to geo-rectified output, is designed to happen entirely in orbit, producing usable intelligence files — GeoTIFF and GeoJSON formats — without touching the ground.

Planet says this technology will scale across its Pelican and forthcoming Owl constellations, building toward what the company describes as a near-real-time global intelligence network.

-0-

The FCC has a proposal on the table that commissioners themselves are calling “Weird Space Stuff” — and that name tells you something about how fast the space industry has moved beyond what regulators were originally built to handle.

At its March meeting, the FCC unanimously approved a Notice of Proposed Rulemaking — an NPRM — seeking public comment on a proposal to make additional spectrum available for the command and control of spacecraft that support emergent space operations but don’t use spectrum as part of any radiocommunications services provided to the public. Think commercial lunar missions. Think novel orbital platforms that don’t fit neatly into the old geostationary or LEO categories.

This week, I sat down with FCC Space Bureau Chief Jay Schwarz to talk through the proposal — and to take a broader look at how the bureau is trying to keep pace with an industry that is moving faster than any regulatory framework was designed to handle.

Schwatz explained that the “Weird Space Stuff” NPRM and the agency’s broader “licensing assembly line” initiative aren’t separate ideas — they’re two parts of the same agenda.

“We as a government, we as Space Bureau, need to scale our operations to match the speed and innovation cycles of what we’re seeing in the industry. So we got to reflect that in government. And so the licensing assembly line is meant to do that, to provide greater speed, greater predictability, and greater flexibility for the industry so that they can get their licenses. We can still do our regulatory duties, but we can do it in a much, much faster and efficient way. And so that’s the part 100 licensing assembly line,” Schwarz said. “The weird space stuff is kind of another piece on this innovation agenda of making sure there’s enough spectrum. Now, where they come together is we did propose in our licensing assembly line something which we call a VTSS or a variable trajectory spacecraft system. And what we’re trying to do here is we’re trying to recognize that as these new activities that we’ve been talking about in this call, as these new activities get out there, we need to make sure that there’s a way to license them clearly.”

A variable trajectory spacecraft system — V-T-S-S — is essentially a new licensing category designed to accommodate missions that don’t follow a fixed, predictable orbit. The kind of mission profile that simply didn’t exist in meaningful numbers when the current rules were written, but that is showing up in application queues with increasing regularity.

The NPRM is open for public comment following publication in the Federal Register. The full interview is available now on The Journal of Space Commerce podcast — which you can find on on Substack, Spotify, Apple Podcasts, YouTube, Rumble, and many other multimedia platforms.

-0-

The FCC Space Bureau chief described the demand for spectrum as, quote, “enormous” — driven by the enormous prosperity that commercial space activities promise to deliver. That spectrum scarcity is precisely what is driving the biggest consolidation story in the commercial satellite sector right now: Amazon’s reported nine-billion-dollar play for Globalstar. [Paywall]

On April 1st — and yes, it was April Fool’s Day, but this was no joke — Globalstar’s stock surged more than 24 percent to an 18-year high on reports that Amazon was in advanced talks to acquire the satellite operator for approximately nine billion dollars. The deal was first reported by the Financial Times and confirmed by Reuters.

This is not, at its core, a satellite story. It is a spectrum story.

Here’s why: Amazon’s LEO broadband constellation — known as Amazon Leo — had approximately 241 satellites in orbit as of early April, following a launch on April 4th that added 29 more spacecraft. Amazon officially operates the third-largest satellite system in orbit and has committed approximately 17 billion dollars in total constellation capital expenditure. But the company faces a hard deadline: the FCC has set a milestone requiring 1,616 satellites in orbit by July 30, 2026. As of right now, that’s roughly 1,375 more satellites in under four months. That gap is the number sitting on every serious Amazon Leo watcher’s desk.

And Amazon cannot buy its way out of that deployment challenge with the Globalstar deal. But what it can buy is something arguably more valuable on a longer timeline: Band n53 spectrum — spectrum that is already internationally coordinated, already commercially deployed, and already generating revenue through a landmark partnership with Apple. Every newer iPhone with emergency SOS capability runs on Globalstar’s spectrum. Amazon would not just be acquiring a satellite company. It would be acquiring a direct-to-device distribution channel already embedded in hundreds of millions of consumer devices.

The acquisition thesis has three legs. First, spectrum that cannot be manufactured or replicated on any short timeline — the FCC’s own spectrum abundance rulemaking proposes 20,000-plus megahertz of new allocations across four bands, but those are years from commercial deployment. Globalstar’s Band n53 is available today. Second, the Apple relationship — though that comes with significant complexity, since Apple holds roughly 20 percent of Globalstar’s equity and has presumptive change-of-control rights. And third, an existing, revenue-generating satellite network: Globalstar turned profitable in 2025 with approximately 273 million dollars in revenue — a real income statement, not a projection.

But there are real risks here, and they deserve the same attention as the strategic rationale.

First, the valuation gap. At nine billion dollars, Amazon is paying a significant premium. Stripped of the Apple contract, the spectrum strategic premium and the acquisition halo, Globalstar’s underlying asset base does not obviously justify that price. And the Apple contract terms — renewal conditions, exclusivity provisions, change-of-control rights — are not publicly disclosed.

Second, the regulatory timeline. Any acquisition of Globalstar requires FCC approval of the spectrum license transfer. As Jay Schwarz noted in our podcast conversation this week, the FCC is navigating competing priorities: promoting competition, supporting the space economy, and managing a regulatory calendar that does not bend to deal timelines. A review measured in quarters rather than weeks creates real execution risk for Amazon — particularly against that July 30th deployment milestone.

Third, the integration architecture problem. Globalstar’s existing constellation runs on fundamentally different orbital parameters, ground infrastructure and spectrum coordination frameworks than Amazon Leo’s purpose-built design. Companies that have navigated similar integration challenges have consistently reported that the timeline exceeded the deal timeline. For Amazon, which is already running hard against an FCC clock, that is a risk that doesn’t appear in any of the headline deal rationale.

One more dimension worth watching: SpaceX. MarketWatch reported on April 2nd that SpaceX may also have interest in Globalstar. If SpaceX is circling this asset, it’s not for the legacy constellation — it’s for Band n53 and the Apple pipeline. A competitive bid from SpaceX would not just raise the price. It would reprice the standalone spectrum valuation of every direct-to-device-adjacent asset in the satellite broadband sector.

The next hard data point arrives soon. AWS first-quarter 2026 earnings are expected in April or May. Watch the AWS segment reporting carefully. Any revenue language referencing connectivity services, satellite broadband or external commercial infrastructure licensing will be the earliest quantitative signal of Amazon Leo’s commercial traction — and the earliest read on what a nine-billion-dollar spectrum acquisition might actually be worth.

You can read the full analysis on The Journal of Space Commerce under the “In Depth” tab. Premium articles this week include a look at one critical factor defining commercial space economics through 2028, and yes Starship is involved, what the 30-moon-landing target actually signals for the Commercial Lunar Payload industry, and why the headline figure of NASA’s DOGE contract cancellations understates the real exposure.

You Might Have Missed

VA268 Mission Will Be the Second Ariane 6 Launch for Amazon Leo

Satellite-derived Agricultural Intelligence Integrates Historical Data

Starfish Space Series B Round Raises Over $100 Million

Redwire Expands European Footprint

Workforce After the DOGE Wave [Paywall]