The NASA Station Award That Cannot Slip

What CLD Phase 2 Means for Supply Chain Leaders Before Summer 2026

What This Means

NASA’s Commercial Low Earth Orbit Destinations (CLD) Phase 2 program was formally placed on hold on January 28, 2026 while the agency aligned the acquisition timeline with revised program requirements. That administrative pause did not stop supply-chain motion: Axiom has pressurized module hardware in fabrication at Thales Alenia Space, Vast moved Haven-1 into integration in Long Beach, and Starlab advanced its primary-structure production path through Vivace. For investors, government buyers, and industrial-base suppliers, the operative signal is straightforward: the companies willing to carry pre-award production risk are positioning themselves to absorb a summer 2026 award faster than rivals still waiting for solicitation certainty.

The Hold That Matters Less Than the Hardware

On January 28, 2026, NASA Johnson Space Center procurement issued a notice stating that CLD Phase 2 was on hold pending alignment with updated program requirements. No Announcement for Proposals had been released as of early 2026, and the earlier April 2026 award expectation effectively slipped out of view.

The more consequential development came earlier, when NASA restructured the acquisition approach away from the previously planned firm-fixed-price Federal Acquisition Regulation (FAR) contract and toward funded Space Act Agreements (SAA) with milestone-based payments. NASA documentation and procurement tracking indicate that the agency still targets summer 2026 for awards and prefers multiple awardees rather than a single winner, a structure designed to reduce the risk of a post-International Space Station (ISS) capability gap.

That means the real competition is no longer about who can brief the best architecture. It is about which team has already activated fabrication, supplier commitments, testing schedules, and integration sequences that can survive a compressed award-to-operations timeline.

Competitor Positioning

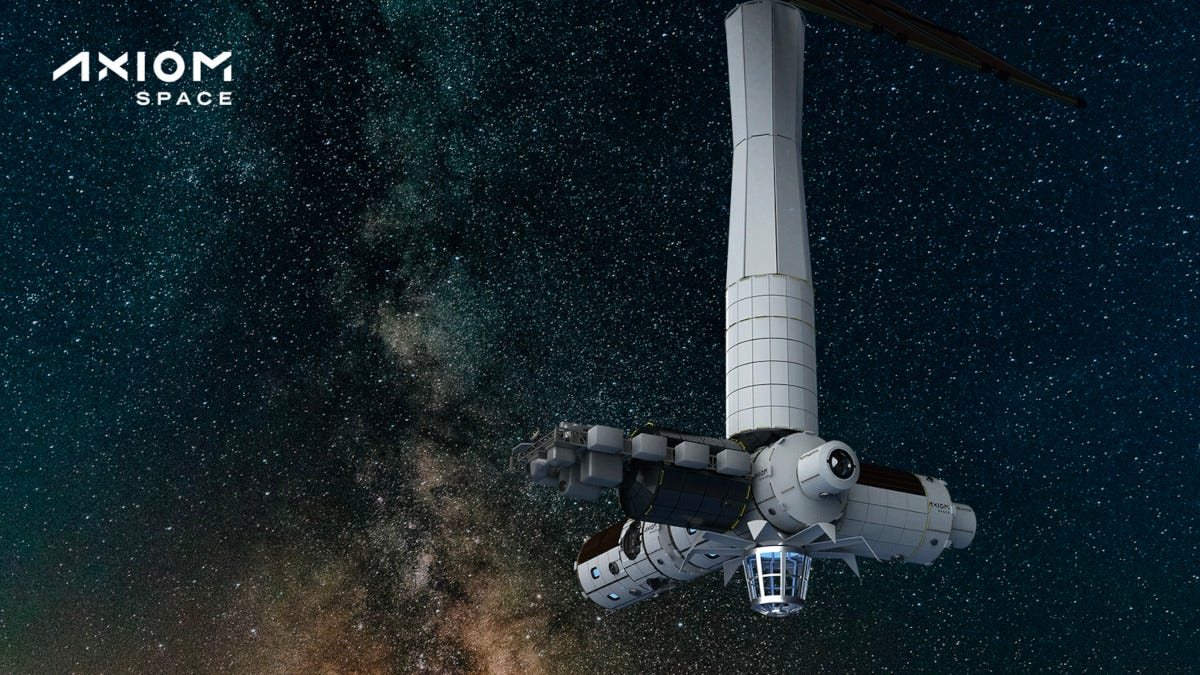

Axiom Space

Axiom Space remains the clearest case of visible hardware progress. Thales Alenia Space announced in 2021 that it would provide the first two pressurized modules for Axiom Station, and Axiom said in December 2024 that Thales Alenia Space was fabricating the primary structure for the Axiom Pressurized Performance and Technology Module in Turin. Axiom also said module assembly activity was advancing toward shipment to Houston, giving the company one of the most tangible station-production signals in the field.

Axiom’s position is strengthened by its ongoing ISS mission activity, including a NASA-backed private astronaut mission planned for 2027 that gives the company a nearer-term operational bridge than some competitors. The supply-chain tradeoff is concentration: Thales Alenia Space is a named Tier 1 pressurized-structure dependency, so any disruption in Italian fabrication, logistics, or schedule performance would transmit directly into Axiom’s station timeline.

Vast

Vast has the sharpest near-term execution signal. The company said in January 2026 that Haven-1 had entered integration in Long Beach, with early work focused on thermal control, life support, propulsion plumbing, tanks, and structural installation before later phases covering avionics, guidance, navigation and control, and air revitalization systems. JSC’s April 2026 integration watch also described Haven-1 as moving through a real build sequence rather than a conceptual campaign, with environmental testing at NASA’s Neil Armstrong Test Facility standing out as a critical gate for schedule confidence.

Space News reported in March 2026 that Vast had raised $500 million to advance Haven-class development, and the company confirmed the raise in a corporate statement the same month, reinforcing that it is committing capital to supply-chain activation ahead of a CLD Phase 2 decision — with specific allocation toward Haven-1 integration infrastructure and long-lead procurement. That makes Vast attractive as an execution story, but it also means suppliers tying themselves to the Haven path are accepting pre-award program risk in exchange for earlier positioning.

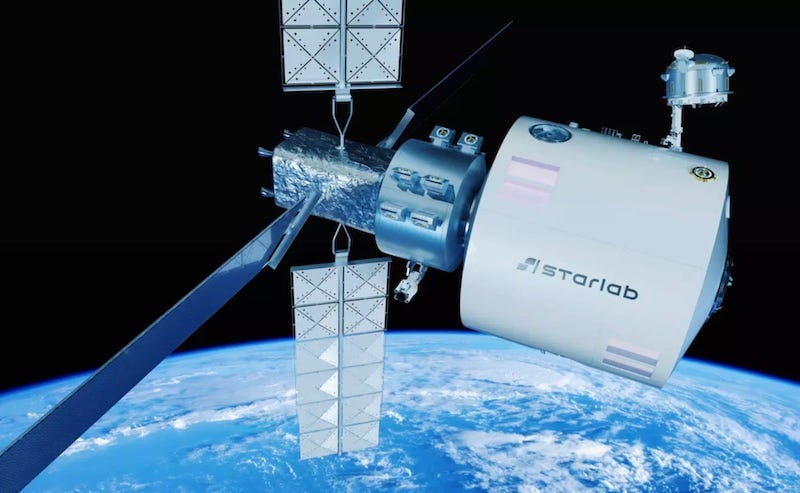

Starlab

Starlab’s competitive strength is consortium depth paired with incremental manufacturing progress. Voyager Space and Airbus finalized the Starlab joint venture in January 2024, establishing a program backed by international industrial and capital partners rather than a single emerging-space company. In September 2025, Voyager said Vivace would lead primary-structure work for Starlab, moving the station from concept maturation into design-to-manufacture and production activity.

That breadth cuts both ways. A transatlantic and multi-partner structure can improve resilience and commercial reach, but it also creates a more complex supply chain with additional coordination, export-control, and integration-management burdens than a simpler domestic architecture would face.

Orbital Reef

Blue Origin’s Orbital Reef remains part of the serious post-ISS field, but publicly confirmed fabrication detail is thinner than it is for Axiom, Vast, or Starlab. That does not mean Orbital Reef is out of contention. It means sub-tier suppliers and business development teams currently have less Tier 1 visibility into where hardware commitments, testing flow, and supplier selection are most advanced.

Readers tracking Orbital Reef should monitor three specific signal categories to close that gap: Blue Origin facility activity at its Kent, Washington manufacturing campus; any SAA milestone filing disclosures in NASA procurement records; and named supplier announcements in avionics integration, life-support heritage systems, and docking interface hardware, which are the sub-tier categories most likely to surface in pre-award program communications. The appearance of named Tier 1 or Tier 2 suppliers in any of these categories would materially upgrade the public supply-chain picture.