The Federal Communications Commission has updated the rules governing how geostationary and non-geostationary satellite systems share spectrum. The Commission voted 3-0 on April 30 to approve a Report and Order that replaces a framework dating back to the late 1990s. That old framework was known as Equivalent Power Flux Density, or EPFD.

The problem is that the satellite market no longer looks like it did in the 1990s.

Modern broadband constellations can change signal behavior in real time, based on link conditions. The FCC’s new approach moves toward performance-based protection criteria, rather than fixed limits built for an earlier technical era.

The Commission says the change could unlock as much as seven times more capacity for space-based broadband and generate more than 2 billion dollars in economic benefits.

But the regulatory point is only half the story. The commercial point is that the FCC is clearing more operating room for satellite broadband to compete directly with cable, wireless and other terrestrial providers. FCC Chairman Branden Carr said at the April 30th meeting that the new rules will benefit consumers.

“Today’s FCC decision will help supercharge that competition while expanding our country’s technological leadership,” Carr said. “Even though high-speed next-gen satellite services provide essential connectivity across the country already, Americans are now about to see a big upgrade. With today’s decision, Consumers could see a seven-fold increase in capacity for these high-speed satellite offerings.”

The decision keeps pressure on private agreements and good-faith spectrum sharing. But it moves the center of gravity away from old technical caps and toward actual performance outcomes.

For executives, investors and program managers, that is the signal to watch. Spectrum policy is now a direct driver of capacity, pricing and market entry.

-0-

Two new market reports this week tell the same broad story from different ends of the satellite business.

One looks downstream, at satellite-based Earth observation. The other looks upstream, at propulsion. Together, they show where demand is growing and where the supply chain may come under stress.

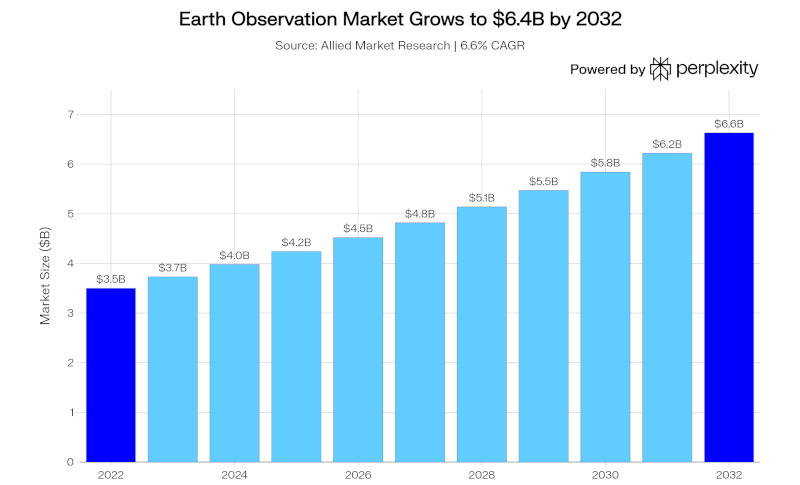

First, Earth observation. According to Allied Market Research, the global satellite-based Earth observation market is projected to grow from $3.5 billion in 2022 to $6.4 billion by 2032. That is a compound annual growth rate of 6.6 percent.

The demand drivers are familiar, but stronger: agriculture, urban planning, disaster management, climate monitoring and defense. Government procurement is still doing a lot of the heavy lifting, with NASA, NOAA and the National Geospatial-Intelligence Agency all buying more commercial data and analytics.

The market is also shifting from raw imagery toward services. Observation-as-a-service, subscription imagery, on-demand tasking and AI-assisted analytics are becoming the more valuable layers.

That is the downstream signal.

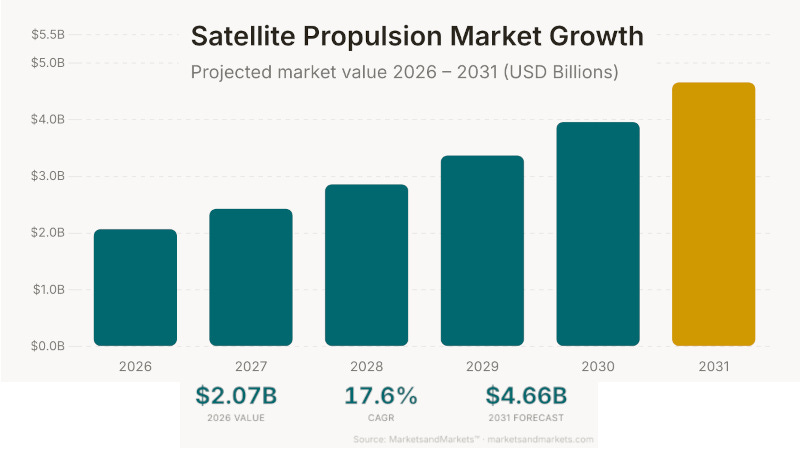

The upstream signal is propulsion. A MarketsandMarkets analysis projects the global satellite propulsion market will grow from a tweak over $2 billion in 2026 to $4.66 billion by 2031. That is a 17.6 percent compound annual growth rate.

The reason is simple. Satellites are not passive hardware once they reach orbit. They need propulsion for orbit raising, station keeping, collision avoidance, repositioning and controlled deorbiting. Electric propulsion is expected to be one of the strongest growth areas because it lowers propellant mass and fits constellation economics.

But there is a caution inside the growth number. Market size does not equal supplier depth. A market can grow quickly and still be constrained by manufacturing capacity, qualification timelines and a limited base of flight-proven providers.

That is why these two reports should be read together. Earth observation growth means more demand for analytics and more government reliance on commercial data. Propulsion growth means more demand for the hardware that keeps satellites maneuverable.

All of that points to value moving toward companies that can connect data, hardware, operations and procurement into something customers can use.

-0-

Next, we turn from market reports to the organizations that help hold the industry together.

Space Foundation was established in 1983, and for more than 40 years it has played the role of convener across the global space community.

It does not build rockets. It does not operate constellations. Its job is to build the ecosystem around the companies, agencies, investors and international partners that do.

That role is easy to understate until the industry gets complicated.

Right now, the industry is dealing with Artemis, Golden Dome, national security space, commercial stations, proliferated constellations and harder questions about international partnerships.

Rich Cooper, vice president of Strategic Communications and Outreach at Space Foundation, made that point in a conversation on The Journal of Space Commerce podcast.

“I will say the state of relationships between international partners, who can do what, who is prepared to do what. Obviously, there’s a lot of challenge that’s going on in the world and lots of debate and discussion about what those alliances are and what they may look like in the future,” Cooper said. “But what you also, I would say, saw is relationships that have been built over decades. literally decades of collaboration and cooperation on countless numbers of missions. Those relationships remain as strong today as they were before. And that’s what gives, I would say, a great deal of energy to this community that we know we can do hard things. We know it’s going to take some challenge. We know that there are going to be some obstacles, but we know together we can get there. Artemis II proved that when you have all of the various pieces that came together and it all worked perfectly.”

The point being that Space commerce is not just a collection of contracts. It is also a relationship network. It depends on which agencies trust which suppliers, and which international partners can still coordinate when politics get hard.

The launch vehicles, the spacecraft and the payloads are visible. The trust network is more behind the scenes. But when programs become multinational and span multiple decades, the trust network becomes a very important part of the operating infrastructure.

A piece of the American launch stack is changing hands again. AE Industrial Partners is taking a majority stake in Rocketdyne’s upper-stage propulsion assets from L3Harris Technologies in an 845 million dollar carve-out. AE Industrial Partners will acquire 60 percent. L3Harris will retain roughly 40 percent. (Paywall)

AE Industrial Partners Managing Partner Kirk Konert told Ex Terra Media just after the acquisition was announced that the company was proud to be restoring a legacy name to the rocket propulsion market.

“It’s been part of every lunar mission since the US started going to the moon and bringing humans to the moon and coming back to the moon this year. We’re really excited to be part of part of that in partnership with NASA and national security programs. And it’s I think it’s a really interesting model as we think about what’s happened with consolidation of all their aerospace and space companies over the last a few decades,” Konert said. “And now what we’re seeing is more of a deconsolidation and new entrants being being introduced into the market. This is part of part of that theme in a new way, which where L3 a prime has been part of the consolidation over the last couple of decades is now partnering with a specialized investor like AE industrial to reinvigorate and standalone a new platform in Rocketdyne, which includes some of the key workhorses of propulsion for our space and national security programs in the U.S.”

The assets include the RL10 upper-stage engine, in-space propulsion systems, nuclear power assets for exploration missions and launch avionics. The RS-25 engine business is not part of the deal.

The RL10 is the center of this story. It powers the Centaur V upper stage on United Launch Alliance’s Vulcan Centaur. That vehicle is tied to National Security Space Launch missions, including payloads for the National Reconnaissance Office, GPS Block III and Wideband Global SATCOM.

That means this is not just another aerospace carve-out. It touches national security launch and the long-term industrial base behind upper-stage propulsion.

AE Industrial Partners has said it wants to apply modern manufacturing discipline to the RL10 production line. That could mean additive manufacturing, better throughput and relief for a constrained supplier base.

But the ownership question matters.

Private equity operates on return horizons. National security launch programs operate on long-term infrastructure commitments. Those timelines can coexist, but they are not the same.

And engine substitution is not easy.

Upper-stage engines are tightly integrated into vehicle architectures. Qualifying an alternative engine for Centaur V could take two to three years of testing and integration work.

If RL10 production improves, the deal could strengthen a critical piece of launch infrastructure.

If ownership incentives or exit timing create disruption, customers do not have a simple procurement detour.

For program offices, investors and primes, the question is whether the owner can steward an engine line that national security customers still depend on.

-0-

Previously, we talked about a satellite propulsion market forecast showing growth from just over $2 billion in 2026 to $4.66 billion by 2031. Those numbers sound healthy. But a separate supply-chain analysis asks a harder question: who is actually going to build all the thrusters the market assumes will be available? (Paywall)

The answer may be thinner than the growth charts suggest.

Novaspace has forecast 16,900 small satellite launches through 2035. Analysys Mason has projected more than 36,000 constellation satellites launching between now and 2034.

But according to the analysis, fewer than a dozen manufacturers can deliver radiation-tested, low Earth orbit-qualified thrusters at the scale implied by that demand.

That is the gap.

Demand is rising. The supplier map says the open-market base may not be deep enough. And that base is getting narrower as constellation operators buy propulsion companies for internal use.

Muon Space acquired Starlight Engines in April. For Muon, that may be a smart hedge. For everyone else, it removes one more independent propulsion supplier from the open market.

This is how supply-chain pressure often shows up before it becomes obvious. The first sign is not always a failed program. Sometimes it is vertical integration. Sometimes it is a supplier that used to be available to the market becoming captive to one customer.

Golden Dome adds another layer. The 2028 demonstration deadline will increase demand for hardware that can survive low Earth orbit radiation environments and fit constellation production schedules.

For program managers, the action item is straightforward: validate secondary sourcing before the bottleneck becomes a schedule problem.

For investors, aggregate market growth is useful, but supplier concentration is where the risk and opportunity sit.

This is why the propulsion story is not only a market-size story. It is a capacity story, a qualification story and a make-or-buy story.

-0-

Finally this week, another supply-chain map has changed, this time in optical intersatellite links. (Paywall)

Rocket Lab closed its $155.3 million acquisition of Mynaric AG on April 14. That deal brought Mynaric’s Munich-based CONDOR Mk3 and HAWK terminal lines into Rocket Lab’s space systems portfolio.

The acquisition matters because optical intersatellite link terminals are not a broad, commodity supplier market. They are a narrow, program-critical piece of the Space Development Agency’s Proliferated Warfighter Space Architecture.

As SDA demand accelerates toward Tranche 2 and Tranche 3 deployments, the supplier map matters. The publicly documented SDA-qualified terminal base runs through four named providers: Mynaric, now under Rocket Lab; Tesat-Spacecom U.S.; Skyloom; and CACI.

That is a short list.

Mynaric began volume production of the CONDOR Mk3 in the first quarter of 2024, but production was not clean. Rocket Lab says it plans to expand capacity, but the public details remain limited.

That means if your program, investment thesis or supplier strategy still treats Mynaric as a standalone company, your map is out of date.

Rocket Lab is now a more vertically integrated space systems company with a meaningful position in optical terminals. That may improve scale over time. It may also change how customers view dependency risk.

This is the same pattern we saw in propulsion. Narrow supplier base. Rising government demand. Vertical integration. Capacity plans that need to be tested against production history.

The market headline is consolidation. The operating question is whether the remaining supplier base can scale quickly enough.

You Might Also Like (Paywall)

The $613 Billion Industry the World Doesn’t Understand

Vertical Integration Is Now a Valuation Story

The Hidden Cost of Telling the Space Story Badly