America’s space industry is booming — but the supply chain keeping it aloft is buckling under the pressure.

A new report from the Aerospace Industries Association and PricewaterhouseCoopers is sounding the alarm: the U.S. space industrial base was built for a different era, and it’s struggling to keep pace with explosive demand.

Consider this — more than 3,400 U.S. space objects were launched in 2025 alone, nearly ten times the volume seen back in 2019. But the factories, suppliers, and testing facilities needed to sustain that growth? They haven’t scaled with it.

The report finds that many critical components are supported by just three or fewer qualified domestic suppliers — and those suppliers are competing against larger industries for the same limited parts. The result: delays across major programs, rising costs, and fragility across the entire chain. AIA Vice President for Space Steven Jordan Tomaszewski said during a webinar discussing the report that there is no silver bullet for solving the supply chain issues.

“It is a number of consistent lines of effort that a lot of times require government and industry to work together on. And not just, but there are some things industry can do on their own, certain things that government can do to have better visibility and to kind of work and help make strategic investments at time or modify policies and regulations,” Tomaszewski said. “So it’s not going to be a fully comprehensive list of all the things that we can do, but hopefully this will be a good roll up for folks just to understand where those pain points are, but then also how we can fix it working together.”

Budget instability and inconsistent government demand signals are also discouraging the private investment needed to expand capacity. Smaller firms are being squeezed by regulatory and cybersecurity burdens they can barely afford to meet.

The fix, according to the report, requires action on multiple fronts — better coordination between government and industry on long-term planning, easing outdated qualification requirements, expanding shared testing infrastructure, and creating financial incentives to bring more suppliers online. Tomaszewski said that 2026 will be the ‘year of the supply chain’

“There’s a lot of government and commercial interest of looking at what the problems are and how do we kind of make things better, which is great. And I think this study really is getting out to some of those specifics,” he said. “What’s that next level down? Okay, we can’t scale up production because these are kind of some of the bottlenecks right now. And then, you know, how do we start getting into the implementation phase of some of these recommendations?”

Eric Fanning, AIA president and CEO said that a resilient space supply chain isn’t optional — it’s a national imperative. The question now is whether Washington and the industry will act before today’s bottlenecks become tomorrow’s crisis.

Steve Tomaszaewski is scheduled to be a guest on a future episode of The Journal of Space Commerce podcast.

-0-

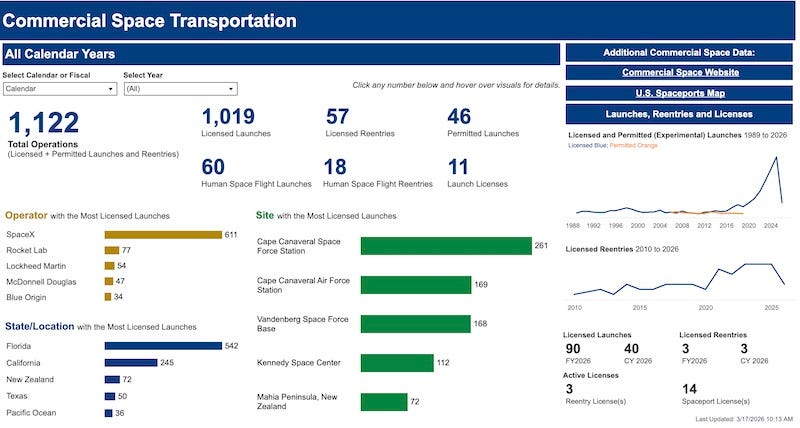

The Federal Aviation Administration has now fully consolidated commercial launch and reentry licensing under Part 450, retiring four older rule sets and moving operators onto a single performance-based framework. The agency’s aim is fewer duplicative approvals, more flexibility in how companies demonstrate safety, and less administrative burden on both industry and government.

Part 450 allows a single license to cover multiple vehicle configurations, different mission profiles and operations from multiple launch and reentry sites all under one authorization, rather than a patchwork of separate approvals. Operators like Blue Origin, Firefly, SpaceX, Rocket Lab, and United Launch Alliance have now transitioned existing licenses ahead of a March 2026 deadline.

For launch providers, the shift has two big consequences. First, it can materially shorten the time from contract signature to first launch, assuming internal teams can keep pace with more compressed data requests from the FAA. Second, it gives operators more room to iterate on vehicles and mission profiles without going back to square one on licensing every time they tweak a configuration.

For satellite operators and investors, the message is that regulatory friction is less likely to be the pacing item than hardware and integration. If launch licensing uncertainty had been a reason to hold back on certain business models, this rule set removes at least part of that excuse.

-0-

York Space Systems has agreed to acquire Orbion Space Technology, a Michigan-based manufacturer of Hall-effect electric propulsion systems designed for constellation-scale missions. Orbion’s Aurora thrusters are already flying on York-built spacecraft, including platforms that support U.S. national security missions.

On the surface, it is a classic supply-chain move: lock in a critical vendor by bringing it in-house.

The deal reduces York’s exposure to external propulsion delays at the very moment that demand for maneuverable LEO spacecraft is accelerating.

Orbion will operate as a wholly owned U.S. subsidiary, continuing to serve a broader set of customers while giving York preferred access and tighter design integration.

But the timing matters. The acquisition comes only weeks after York’s initial public offering, which raised hundreds of millions of dollars and positioned the company more explicitly as a Tier 1 defense and commercial prime. Analysts project rapid revenue growth, and integrating propulsion directly into York’s platform roadmap is a way to support that scale without getting trapped in the same long lead times that are hitting other primes.

For the rest of the ecosystem, this is part of a broader pattern. Prime contractors are using balance-sheet capital to secure scarce capabilities, from propulsion to optics. Smaller operators that once counted on shared suppliers may now find those vendors sitting behind a prime’s firewall or booked out by long-term framework agreements.

Propulsion capacity is migrating from open market to captive asset faster than many business plans assumed. That makes early, durable relationships with remaining independent suppliers more important—and raises the odds that additional consolidation is on the way.

Orbit is not just getting crowded with spacecraft—it is getting cluttered with retired hardware. That is opening the door for orbital debris removal as a commercial service, not just a policy talking point.

Astroscale’s planned ELSA‑M in‑orbit demonstration is a good example. Under a new launch agreement with Isar Aerospace, Astroscale will fly a roughly 520‑kilogram servicer designed to rendezvous with and remove an end‑of‑life Eutelsat OneWeb satellite. The mission is majority self‑funded, with additional backing from the UK Space Agency through ESA’s ARTES program as part of the Sunrise public–private partnership with Eutelsat.

Isar will launch ELSA‑M on its Spectrum vehicle from a dedicated pad at Andøya Space in Norway, showcasing both launch flexibility and the orbital precision needed for close‑proximity operations. Spectrum is designed, built, and operated in‑house with a high degree of automation, giving Isar a path to scale production as demand for targeted missions—including debris removal—grows.

For Astroscale, ELSA‑M is the next step on a roadmap that includes earlier missions like ELSA‑d and ADRAS‑J, which demonstrated key skills such as safe approaches, robust relative navigation, and controlled operations near uncooperative objects. ELSA‑M aims to become the world’s first commercial end‑of‑life service for “prepared” satellites, meaning spacecraft designed with interfaces that support docking and removal.

From a space‑commerce standpoint, several points matter:

Debris removal is moving from technology demo to revenue‑generating service tied directly to operators’ lifecycle plans. Launch providers see this as a growth market, building manifest flexibility and orbital targeting into their value proposition for rendezvous missions, and regulators and insurers are watching closely, because routine end‑of‑life services could eventually influence licensing terms, collision‑risk assessments, and premiums for high‑value constellations.

The practical question is whether your satellites are being designed as “customers” for this emerging service layer. If interfaces and end‑of‑life concepts are not being baked into current programs, you could be closing off future options to mitigate debris risk and differentiate on sustainability.

-0-

There are start-ups looking to rethink what “infrastructure” means in orbit, and one of the more speculative ideas gaining attention is the concept of delivering sunlight to shaded or energy-constrained locations on Earth using space-based reflectors or power systems. Among those companies is Mantis Space, which just emerged from stealth with an oversubscribed seed round of more than $10 million. The concept is to place controllable platforms in orbit that can redirect solar energy on demand, extending productive hours for agriculture, industrial operations, or disaster response.

For now, it is early-stage and high-risk.

These concepts run into tough questions around launch and deployment costs, even under a streamlined licensing regime, precision station-keeping and attitude control to keep beams or reflections where they are supposed to be and regulatory and public acceptance, given concerns about light pollution, safety, and potential dual-use implications

But from a supply-chain standpoint, they point in a consistent direction. More complex, persistent infrastructure in orbit increases demand for high-efficiency propulsion to maintain precise orbits, robust optical systems to control and monitor power delivery and reliable, radiation-hardened electronics to manage autonomy at scale.

Those are the same categories already showing stress in today’s supply chain surveys. If even a fraction of these orbital power and sunlight concepts move from pitch deck to deployment, they will amplify the competition for components that defense and commercial operators already struggle to secure.

-0-

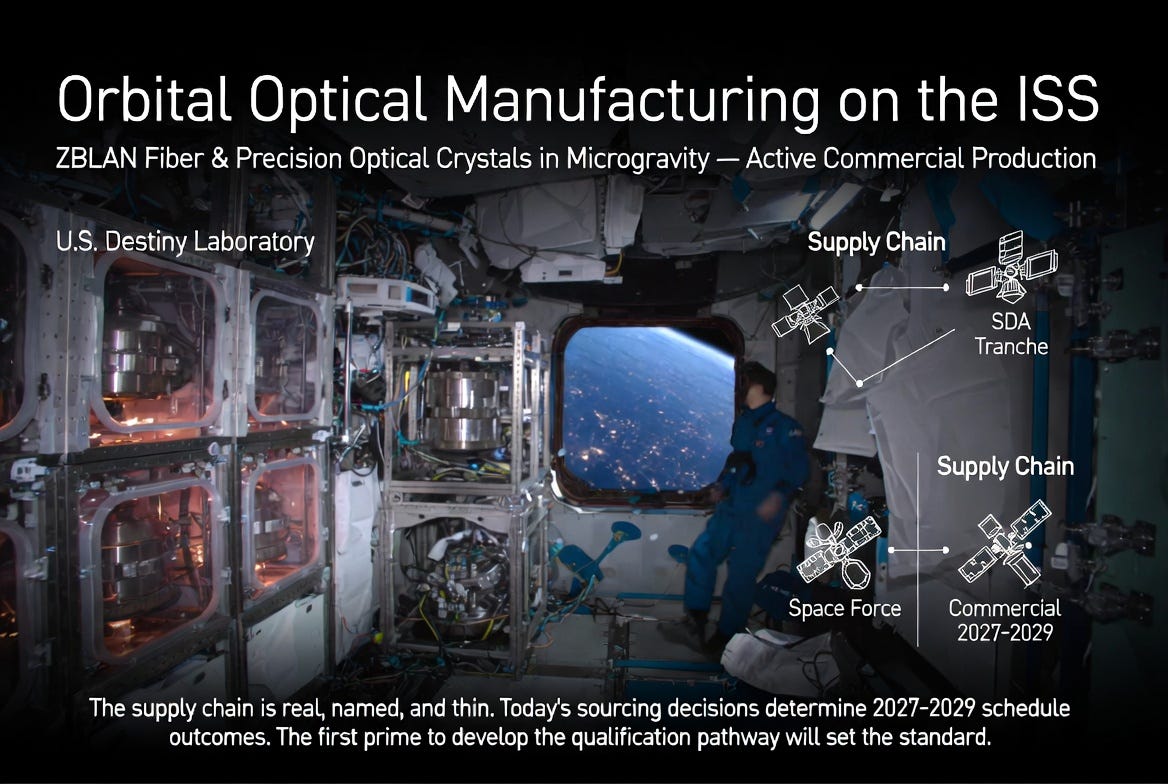

In Depth this week, the “orbital optical gap” that sits between what next‑generation constellations will need from their optical components, and what the current supplier base can realistically deliver from Earth. (Paywall)

Most procurement teams keep a tidy list of approved optical vendors—domestic specialists, a few European houses, and lead times that look uncomfortable but accepted. What almost none of those lists include is an orbital address, even as governments and defense agencies start placing directional bets on optical manufacturing in microgravity.

In February, the UK Space Agency awarded about 295,000 pounds to British start‑up OrbiSky to design a payload for producing ZBLAN fluoride glass optical fiber in low Earth orbit. That follows ESA’s decision to name ZBLAN a priority in its Advanced Materials and In‑Orbit Manufacturing program, Varda Space Industries returning a U.S. Navy research payload on its W‑5 mission, and the Air Force Research Laboratory’s continued work with Redwire on in‑space manufacturing. Taken together, those moves signal that orbital optical production is no longer a lab curiosity—it is becoming a capability governments expect to use.

The physics are what make this different.

ZBLAN fiber can, in theory, deliver 10 to 100 times lower signal loss than silica over key portions of the spectrum, which is a system‑level advantage for high‑bandwidth optical intersatellite links. On Earth, gravity-driven convection and sedimentation create microcrystals during fiber drawing, scattering light and destroying that performance; experiments dating back to NASA parabolic flights in the 1990s showed that even brief microgravity reduces crystal formation, and sustained orbit is where ZBLAN can approach its theoretical best. That means terrestrial process improvement cannot fully substitute for making this material in space.

So what does the orbital optical supply chain actually look like today?

The ISS model: Redwire, through its Enhanced In‑Space Manufacturing facility, has been producing optical crystals and fiber commercially on the International Space Station and reported the first sale of a space‑manufactured optical crystal in 2022. Flawless Photonics has run an autonomous ZBLAN platform on ISS, delivering nearly 12 kilometers of fiber to the University of Adelaide by early 2025, while earlier players like Physical Optics and FOMS demonstrated precursor hardware.

The free‑flyer model: Varda’s W‑series spacecraft use Rocket Lab’s Photon bus and a reentry capsule to process materials in orbit and bring them home, with the W‑5 mission under AFRL’s Prometheus program proving both cadence and reentry for defense customers ahead of crystal‑manufacturing payloads. Varda has also signed a joint development deal with United Semiconductors for orbital crystal production, signaling early commercial demand.

New entrants: OrbiSky’s UKSA‑funded SkyYield study, ESA’s ZBLAN prioritization, and Flawless Photonics’ expansion into Luxembourg all point to a growing European footprint, with implications for ITAR, export controls, and industrial policy.

The problem is scale and timing. Current orbital optical production is measured in kilograms per mission and kilometers of fiber per run, while large constellations are measured in thousands of components across multi‑year builds. ISS itself is on track for decommissioning around 2030, and the commercial LEO destinations meant to replace it do not yet have firm construction and operations timelines, leaving a transition risk for ISS‑dependent providers.

Then there is the qualification gap. No major prime has publicly documented a supplier‑qualification process for in‑space‑manufactured optical components, and no government requirement set yet treats orbital manufacturing as a recognized production path for flight hardware. AFRL’s Prometheus program offers a partial pathway, but it is focused on reentry science and defense materials, not bulk component supply for broadband constellations.

For investors, this looks like a pre‑institutional market: verified government demand, early commercial customers, and no settled capital framework. Redwire reports a growing backlog including advanced manufacturing work, Varda is flying multiple missions under AFRL, and European agencies are backing multiple ZBLAN players with modest but strategic contracts. The satellite manufacturing market, meanwhile, is projected to expand sharply through the early 2030s, with demand for high‑performance optics tracking the shift to optical intersatellite links.

The orbital optical gap is real, the companies working to close it are already flying hardware, and the procurement window for programs that will eventually need their output is opening now.

Paid subscribers can read the full analysis on The Journal of Space Commerce under the Supply Chain tab. Other premium articles this week include an analysis of what the Stargaze from SpaceX signals for the future of orbital governance, and the five component sub-tiers that could define smallsat’s $30 billion decade.