We start with what may be the most closely watched accountability story in human spaceflight in years. NASA has officially released the findings of an independent Program Investigation Team that examined what went wrong during Boeing’s Starliner Crewed Flight Test back in 2024.

Starliner launched on June 5th, 2024, carrying NASA astronauts Butch Wilmore and Suni Williams to the International Space Station. The mission was supposed to last eight to fourteen days. Instead, propulsion system anomalies discovered while the spacecraft was in orbit stretched the mission to 93 days — and ultimately led NASA to make the extraordinary decision to bring the spacecraft home without its crew. Wilmore and Williams eventually returned to Earth in March 2025 aboard a SpaceX Crew Dragon.

Now we know more about why. Investigators found what they describe as an interplay of combined hardware failures, qualification gaps, leadership missteps, and cultural breakdowns — all of which created risk conditions inconsistent with NASA’s human spaceflight safety standards.

NASA Administrator Jared Isaacman said that NASA had allowed “overarching programmatic objectives.”

“Mistakes incurred from program’s inception and continued throughout execution, including contractual management, oversight posture, technical rigor, and leadership decision-making. Boeing built the spacecraft, and from the onset, NASA approved variances, and we agreed to fly it. As development progressed, design compromises and inadequate hardware qualification extended beyond NASA’s complete understanding,” Isaacman said. “Now, variances exist across all major aerospace programs and by themselves are not unusual. The engineering reality, however, is that Starliner, with its qualification deficiencies, is less reliable for crew survival than other crewed vehicles. And that was as noted by the report. But at NASA, we managed the contract. We accepted the vehicle. We launched the crew to space. We made decisions from docking through post-mission actions. A considerable portion of the responsibility and accountability rests here.”

As a result of the findings, NASA has formally classified the Starliner crewed flight test as a Type A mishap — the highest-level classification — citing potential for a significant mishap and the financial damages incurred. No astronauts were injured, and the mission did regain spacecraft control prior to docking. But the classification signals that NASA is treating this with full seriousness.

NASA says it will continue working with Boeing to address the technical challenges before flying Starliner again. The full report — with some redactions to protect Boeing’s proprietary information — is available on NASA’s website.

-0-

Transportation is just one aspect of maintaining a sustained human presence in Low Earth Orbit ... one big question is where will that human presence be when the ISS is retired, possibly as early as 2030.

One of the possible replacement commercial stations is being developed by Starlab Space, and that company marked a significant milestone recently, completing its Commercial Critical Design Review, or CCDR, with NASA in attendance. This marks a decisive transition: the program is moving from the design phase into manufacturing and systems integration. In milestone terms, it satisfied the 28th checkpoint on Starlab’s NASA Commercial LEO Destinations Space Act Agreement — a mouthful, but what it means in plain English is that Starlab has demonstrated its design is technically mature, integrated, and ready to be built.

According to Starlab CEO Marshall Smith, the CCDR is a critical step toward delivering that continuous access to Low Earth Orbit with — his words — “no gap in capability to science, industry or national interests.” He also emphasized that the program’s business plan review was completed in parallel, validating what he called a diversified commercial market rather than a government-dependent model.

The Starlab program draws on a remarkable international coalition of partners, including Voyager Technologies, Airbus, Mitsubishi Corporation, MDA Space, Palantir Technologies, ESA, JAXA, and Space Applications Services.

This is a significant milestone. A lot of things have to go right for humanity to maintain an unbroken chain of human presence in orbit — and Starlab just demonstrated that its piece of the puzzle is executable.

-0-

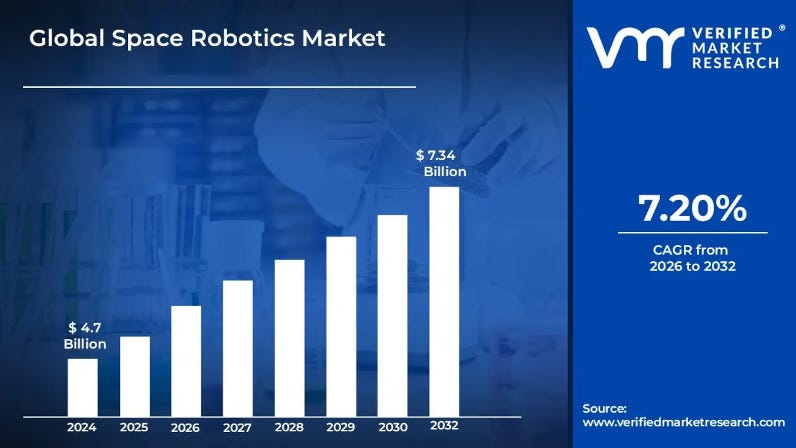

A new report from Verified Market Research finds that the global space robotics market — valued at 4.7 billion dollars in 2024 — is projected to grow to more than 7.3 billion dollars by 2032. That’s a compound annual growth rate of about 7.2 percent over the forecast period.

What’s driving this? A few key forces. First, the increasing complexity of orbital and deep-space missions is accelerating demand for autonomous systems that can perform inspection, assembly, repair, and exploration tasks with minimal human intervention. Second, satellite servicing — including refueling, debris management, and in-space infrastructure maintenance — is creating sustained demand for precision robotic platforms. Third, rapid advances in artificial intelligence, machine learning, and sensor fusion are expanding what robotic systems can actually do, and where they can do it — from low Earth orbit to the Moon to Mars.

The report notes that North America remains the dominant market, led by U.S. government funding, private sector innovation, and a mature aerospace industrial base. Europe is a strong secondary market. And Asia-Pacific is emerging quickly, with China, India, and Japan all expanding their space robotics capabilities.

There are challenges too. Space robotics systems require extensive testing, radiation hardening, and customization for specific missions — all of which drive up costs and development timelines. And robotic failures in space carry serious financial and reputational consequences, which means reliability and redundancy engineering remain critical and expensive.

The Commercial Space Federation has released a new study titled “Perfecting Public-Private Partnerships: The Future of Government Space Contracts,” authored by the policy consultancy Rational Futures. The report is a candid assessment of how NASA, the Department of Defense, and other space agencies structure their commercial relationships — and it argues that many of those agencies are getting it wrong in ways that lead to cost overruns, schedule delays, and missed opportunities.

The core argument is this: agencies too often conflate “public-private partnership” with specific contract mechanisms — particularly firm-fixed-price contracts — without thinking carefully about whether those mechanisms match the actual risk profile of what they’re buying. The report frames procurement on a spectrum from fully government-controlled programs, where the public sector holds all the risk, to fully commercial models, where a private company holds all the risk and sells services to anyone who will buy them. Most space programs sit somewhere in the middle, and the paper argues that matching the right contract type to the right program characteristics is essential.

The study holds up NASA’s Commercial Orbital Transportation Services program — the original COTS effort that incubated SpaceX and Orbital Sciences — as the gold standard of what works: cost-sharing, multiple suppliers, stable requirements focused on outcomes rather than process, and large follow-on contracts that gave investors confidence. By contrast, it looks at the Commercial Lunar Payload Services program as a cautionary tale, citing overly optimistic demand projections, shifting requirements, and inconsistent oversight as contributors to delays and cost growth.

The recommendations span three levels. At the agency level: build internal capacity in finance, economics, legal, and procurement — not just engineering. At the program level: conduct rigorous independent market assessments, signal clear multi-year demand, and avoid over-relying on a single vendor. At the contract level: match the procurement vehicle to where the technology actually is, not where you wish it were.

The report’s authors sum it up this way: “Success requires careful planning, involvement of appropriate experts, and understanding of market conditions and program characteristics.” It sounds obvious. But based on recent history, it’s a lesson the industry apparently still needs to hear.

-0-

This week on The Journal of Space Commerce Podcast, I talked with Dr. Belinda Marchand, the chief scientist at Slingshot Space.

Space has become a critical warfighting domain, requiring an approach to training that prepares warfighters to use new technology. AI is redefining space warfare training, and is becoming vital for deterrence and national security.

Slingshot Aerospace is a U.S.-based space data and analytics company focused on making space operations more safe, sustainable, and secure through satellite tracking, space traffic coordination, and high‑fidelity modeling and simulation tools.

Dr. Marchand said that using AI allows warfighters to train like they’ll fight. But she also said that the technology being used can be applied to commercial scenarios as well.

“I think the defense use case was a very valuable and timely example of a way to demonstrate the capabilities of the technology. But the technology itself that powers things like Talos, or even that powers our anomaly detection software like Agatha or anomalous actor detection, all those technologies can be used for other purposes as well, right?” Marchand said. “You can use them to... fly your fleet to control your fleet, to achieve your on-orbit servicing objectives, anything that involves rendezvous proximity operations. You could adapt. If you’re doing RPOs for intercepting something, that’s not that dissimilar from the type of activity you would do to go service something or refuel something, right? Or to do in-orbit manufacturing and things like that. So the actions have elements in common and the framework itself is agnostic to those actions.”

Slingshot recently achieved Cybersecurity Maturity Model Certification (CMMC) Level 2, validating its ability to protect Controlled Unclassified Information (CUI) in support of Department of Defense (DoD) missions.

-0-

In Depth this week ... the space industry has a new cost of doing business — and it’s not coming from regulators. It’s coming from physics. (Paywall)

A January 2026 World Economic Forum report put a price tag on orbital debris: somewhere between $26 and $42 billion in projected losses over the next decade. No one sends you a bill. But insurance underwriters, propellant budgets, and procurement officials are quietly collecting anyway.

Here’s the situation: Low Earth orbit is crowded. Over 25,000 tracked objects are up there, plus millions of tiny fragments too small to see — but large enough to destroy a satellite. Mega-constellations from SpaceX, Amazon, and others have turned what was once open frontier into a congested operating environment. Satellites are now maneuvering daily to avoid collisions. Every maneuver burns fuel. Less fuel means shorter missions. Shorter missions mean less revenue.

On the regulatory side, the FCC’s new five-year deorbit rule kicked in last September, requiring satellite operators to bring their spacecraft down within five years of mission end. That sounds simple, but it forces a real tradeoff: every kilogram of propellant reserved for deorbit is fuel you can’t use to extend your operational life. And the rule hits smaller operators hardest — SpaceX already operates this way by design, giving them a quiet competitive advantage.

Meanwhile, the insurance market is repricing in real time. Premiums in high-traffic orbital zones are now eating five to ten percent of total mission budgets — and policies increasingly require operators to demonstrate active maneuverability and credible end-of-life plans just to get coverage.

In Congress, the ORBITS Act is pushing toward mandatory active debris removal — not just preventing new junk, but cleaning up what’s already there.

The bottom line for the industry: orbital sustainability has moved from an aspirational goal to a line item on the income statement. The debris tax is already collecting. The only question is whether your financial model accounts for it.

Worth a Second Look

Axiom Space Secures $350M in Financing for Spacesuits, Station

Wildfire Detection Application Onboard AI-enabled Satellite Demonstrated

Satellites Market worth $46.79 Billion by 2031: Report

LambdaVision Books Commercial Space in Low-Earth Orbit

From NASA Customer to Market Anchor (Paywall)