The UK small launch sector is facing a rough moment. Orbex, one of Britain’s most prominent homegrown rocket companies, has filed a notice of intention to appoint administrators after its Series D fundraising round came up empty. Merger and acquisition talks also failed to produce a deal. With no funding lifeline in sight, the company is now formally exploring the sale of all or part of its business.

It’s a painful moment for a company that was genuinely close to something. Orbex had brought hundreds of skilled jobs to Scotland, had been at the vanguard of UK space ambitions, and was on the verge of test flights for its Prime microlauncher later this year. All of that is now in limbo.

But here’s where the story takes a turn. Skyrora — another UK launch company — has stepped forward with an interest in acquiring select Orbex assets, including the Sutherland Spaceport in northern Scotland. Skyrora says it’s prepared to invest up to ten million pounds — roughly thirteen-and-a-half million dollars — subject to due diligence and negotiations with the administrators.

The framing from Skyrora is explicitly nationalistic: keeping UK technology under UK ownership, protecting national infrastructure, and safeguarding the return on taxpayer investment that went into Orbex over the years.

Now, nothing is done yet. Administrators have only just been notified, and the legal process has to run its course. But if Skyrora does pull this off, it would be a remarkable consolidation story — one UK launch company absorbing the assets of another to create something more resilient. The Sutherland Spaceport alone would be a significant prize, as it’s one of the few licensed launch facilities in Europe capable of reaching polar and sun-synchronous orbits.

-0-

A new wave of industrial connectivity could be about to reshape how industries operate in remote and underserved areas — and the timeline is tighter than you might expect.

New research from satellite company Viasat, based on a survey of 600 industrial decision-makers worldwide, finds that 91% plan to adopt direct-to-device satellite technology within the next 18 months. The sectors involved span agriculture, energy, mining, logistics, and utilities — industries where reliable connectivity has long been a limiting factor.

At the heart of this shift is a technology called Narrowband Non-Terrestrial Networks — or NB-NTN — a connectivity standard that allows IoT devices to maintain a satellite link when ground-based networks are unavailable or overstretched. Think of it as a seamless fallback that kicks in without any manual intervention.

The data suggests momentum is already building. 78% of respondents say their IoT deployments have accelerated over the past year — and among organizations already using hybrid satellite-terrestrial setups, that figure jumps to 86%.

Viasat frames this less as a performance upgrade and more as a pursuit of what the report calls “coverage certainty” — the ability to stay connected at scale, regardless of where you are or what the local infrastructure looks like.

The findings also carry a pointed message for mobile network operators: direct-to-device satellite capability shouldn’t be treated as a niche add-on. According to the report, it represents a genuine opportunity to expand into new enterprise revenue streams — without requiring significant reinvestment in existing networks.

-0-

The Idaho National Laboratory just released a report called “Weighing the Future: Strategic Options for U.S. Space Nuclear Leadership”, and it lays out three distinct paths forward.

The first is what the report calls “Go Big or Go Home” — a large-scale, hundred-to-five-hundred kilowatt electric project led by NASA or the Department of Defense. But it’s high risk, high reward, and requires consistent top-level funding and political will.

The second option — dubbed the “Chessmaster’s Gambit” — splits the approach into two smaller public-private projects, both under a hundred kilowatts. One would put a reactor in lunar orbit or on the Moon’s surface. The other would be an in-space system. The appeal here is flexibility — private companies choose the technology, which distributes risk and keeps timelines more manageable.

The third path, “Light the Path,” is the most cautious — a small radioisotope demonstration under one kilowatt, designed mainly to build regulatory frameworks and institutional knowledge before committing to bigger bets.

For context on why this matters: NASA has already issued a directive to place a fission reactor on the Moon by fiscal year 2030. That’s four years away. The technology challenges are real — space reactors have to be lightweight, run at much higher temperatures than terrestrial units, and operate for a decade without maintenance. None of that is easy.

Sebastian Corbisiero, the Department of Energy’s Space Reactor Initiative national technical director, described the moment as potentially being on the cusp of a major step forward for nuclear power in space. And given that competitors — particularly China — are investing heavily in space nuclear capabilities, the pressure to act is real.

Which path the U.S. ultimately chooses will say a lot about its appetite for risk — and its confidence in the commercial sector to deliver.

NASA has selected Vast Space for the sixth private astronaut mission to the ISS. The flight is targeting no earlier than summer 2027, launching on a SpaceX Falcon 9 carrying a Dragon spacecraft. The crew will spend up to 14 days aboard the station.

This is a milestone for Vast, which is best known for its ambitions to build and operate its own commercial space station — the Haven-2 — as a successor to the ISS. A crewed mission to the station is exactly the kind of operational credibility the company needs to make that case.

Vast has framed the mission as part of the broader transition to commercial space stations, and fully unlocking the orbital economy. The science portfolio planned for the mission spans biology, biotechnology, physical sciences, human research, and technology demonstrations.

What’s interesting here is the strategic layering. Vast isn’t just flying to the ISS for the publicity — the company has a live call for research proposals open right now, meaning external researchers can submit experiments for consideration aboard this mission. That’s a signal that Vast is trying to build an actual customer base and research pipeline before its own station even exists.

The ISS is scheduled for deorbit in 2030. Between now and then, these private astronaut missions serve a dual purpose: they generate revenue for NASA and its partners, and they give commercial operators like Vast the hands-on experience they’ll need to run stations on their own.

-0-

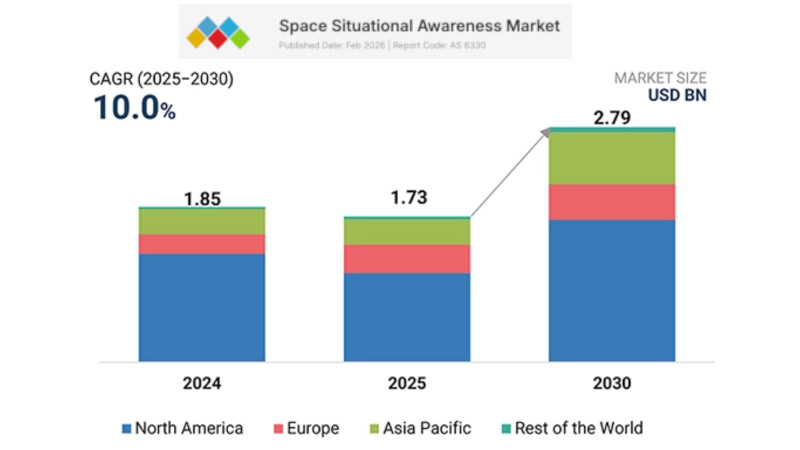

Analysts at MarketsandMarkets are projecting the global space situational awareness market — SSA, for short — will grow from about 1.7 billion dollars in 2025 to nearly 2.8 billion dollars by 2030. That’s a compound annual growth rate of ten percent over five years.

SSA, if you’re not familiar, is the business of tracking what’s in orbit: active satellites, spent rocket bodies, debris fragments, and everything in between. As constellations like Starlink and others pour thousands of satellites into low Earth orbit, the risk of collisions — and the cost of getting it wrong — increases dramatically.

The debris segment is expected to hold the largest share of the SSA market. That tracks. There are hundreds of thousands of debris objects in orbit too small to track reliably but large enough to be catastrophic. Even a centimeter-sized fragment at orbital velocity carries enormous kinetic energy.

Geopolitically, there’s another driver: governments want independent visibility into what’s happening in their orbital neighborhoods. That’s pushing investment in indigenous SSA infrastructure, particularly in the Asia-Pacific region, where China, India, Japan, and South Korea are all expanding their space programs and their appetite for homegrown tracking capabilities.

The major players in this space currently include Lockheed Martin, L3Harris, Kratos, Parsons, and Peraton — all defense-adjacent firms with deep government relationships. But as the market grows, expect more commercial entrants chasing the non-government slice of that revenue. So the bottom line would appear to be that, if you’re operating in orbit, knowing where your spacecraft ... and everything else ... is has never been more important — or more valuable.

-0-

In Depth this week ... The space economy is booming — but not in the way you might expect. Forget rockets and moonshots. The real action right now is in data. Earth observation satellites, geospatial intelligence platforms, and satellite communications networks are driving a steady wave of mergers and acquisitions, and investors are paying serious money to get in. (Paywall)

Deals in 2024 and 2025 are showing revenue multiples in the one-to-four-and-a-half times range, with EBITDA multiples stretching into the teens — healthy numbers that hold up well against broader aerospace benchmarks. The buyers range from defense giants filling gaps in their geospatial portfolios to private equity firms building roll-up platforms around recurring data revenue. The message from the deal tape is clear: space data is now considered core infrastructure, alongside defense, climate monitoring, and global connectivity.

But here’s where it gets complicated. Regulators are catching up — fast. The European Union is advancing a Space Act that would treat certain satellite-derived data much like personal data under GDPR. The OECD is raising red flags about high-resolution imagery being combined with AI to track individuals and sensitive facilities. And the UN’s space office is pushing new principles for responsible AI in Earth observation. The direction of travel is unmistakable: tighter rules on consent, data provenance, and how satellite analytics can be used and sold.

So the billion-dollar question for investors is this — do current valuations already price in the cost of compliance, or are buyers underwriting a more permissive world than regulators will actually allow?

The answer likely splits the market in two. Companies that build privacy and governance into their core architecture are positioned to command premium valuations. Those treating compliance as an afterthought may face multiple compression, heavier deal indemnities, and shrinking revenue streams.

In the space data economy, your data governance framework may soon matter as much as your satellite constellation.

Paid subscribers can read the full analysis on The Journal of Space Commerce under the In Depth tab. Other premium articles this week include how strategic communications will shape the future of the commercial space industry, and the hidden vulnerability in the U.S. space industrial base.

-Ends-

Worth a Second Look

Partnership Will Advance Disaster Management and Prevention

Stoke Space Technologies Extends Previously Announced Series D Financing

Collaboration Aims to Accelerate Access to Space

Thunderbird Station Unveiled by Max Space

AT&T’s $15.6 Billion Satellite Bet (Paywall)