Space Situational Awareness Market worth $2.79 billion by 2030: Report

CAGR of 10.0% Forecast for the Segment

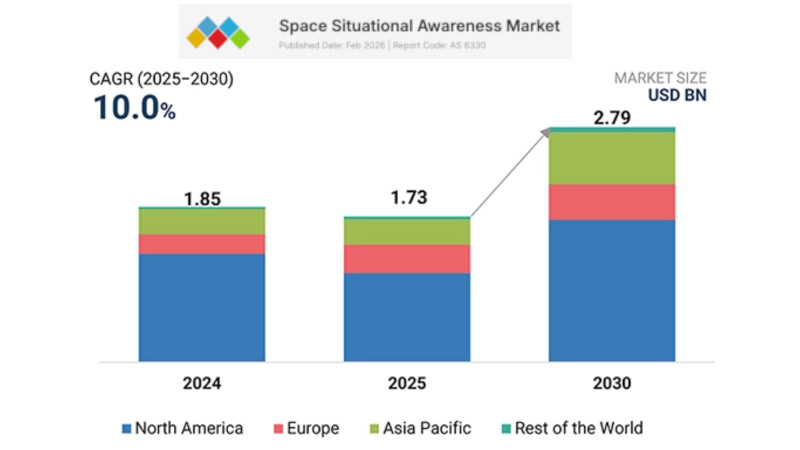

The space situational awareness market is projected to grow from USD 1.73 billion in 2025 to USD 2.79 billion by 2030, at a CAGR of 10.0%, according to a new report from MarketsandMarkets.

The demand for space situational awareness is driven by the rapid increase in active satellites and orbital congestion. Operators are investing more in collision avoidance, anomaly detection, and mission safety as the cost of satellite failure continues to rise. The global market for space situational awareness is being driven by an increasing reliance on space assets for defense, navigation, communications, and disaster response. Additionally, there is heightened geopolitical emphasis on space security, leading governments to seek greater visibility into activities in orbit. This demand is primarily driven by defense and government agencies.

The debris segment is expected to hold the largest share of the space situational awareness industry due to the fast buildup of non-functional satellites, fragments, and launch-related objects in orbit. Even very small debris can pose serious collision risks, forcing operators to track and predict conjunctions regularly. Regulatory pressure on operators to show safe operations is also increasing the need for debris-focused monitoring. Since cleanup and removal missions are still limited, tracking debris remains the main tool for reducing risk.

Near-Earth orbit is expected to experience significant growth due to numerous active satellites, including large Low Earth Orbit (LEO) constellations. The frequent maneuvers of these satellites, combined with heavy traffic and shorter orbital lifecycles, necessitate higher update rates and more precise tracking. As a result, commercial operators are investing in near-real-time space situational awareness (SSA) data to ensure their services run smoothly and avoid disruptions.

Asia Pacific is expected to be the fastest-growing region during the forecast period. This is mainly due to expanding national space programs and increased satellite deployments in countries such as China, India, Japan, and South Korea. Governments in the region are strengthening space security capabilities and have started to invest more in indigenous SSA infrastructure. There is growing commercial launch activity, and regional constellations are increasing local demand for tracking and collision avoidance services. The need to reduce reliance on foreign SSA providers further supports market growth across the region.

Lockheed Martin Corporation, L3Harris Technologies, Inc., Kratos Defense & Security Solutions, Inc., Parsons Corporation, and Peraton are the major players in the space situational awareness companies. These companies have strong distribution networks across regions like North America, Europe, Asia Pacific, and the Rest of the World.