What This Means.

Three companies are currently competing to establish the dominant business model for delivering payloads to the Moon, and they are making structurally different bets about where margin actually lives in the cislunar economy. Voyager Technologies’ acquisition of Astrobotic, Firefly Aerospace’s Blue Ghost mission record, and Astrobotic’s ongoing Griffin program together represent three distinct theories of the business, each with different capital requirements, revenue concentration risks, and dependency on National Aeronautics and Space Administration (NASA) contract flow. Investors and executives allocating capital to the cislunar sector need a framework for evaluating which model survives the transition from government-funded demonstration to commercially self-sustaining operation. Of the three, Firefly’s launch-business hedge is the only structure that currently provides a partial revenue floor independent of Commercial Lunar Payload Services (CLPS) task order timing, though that advantage is partial, not absolute, and the conditions under which it holds are examined in the body of this analysis.

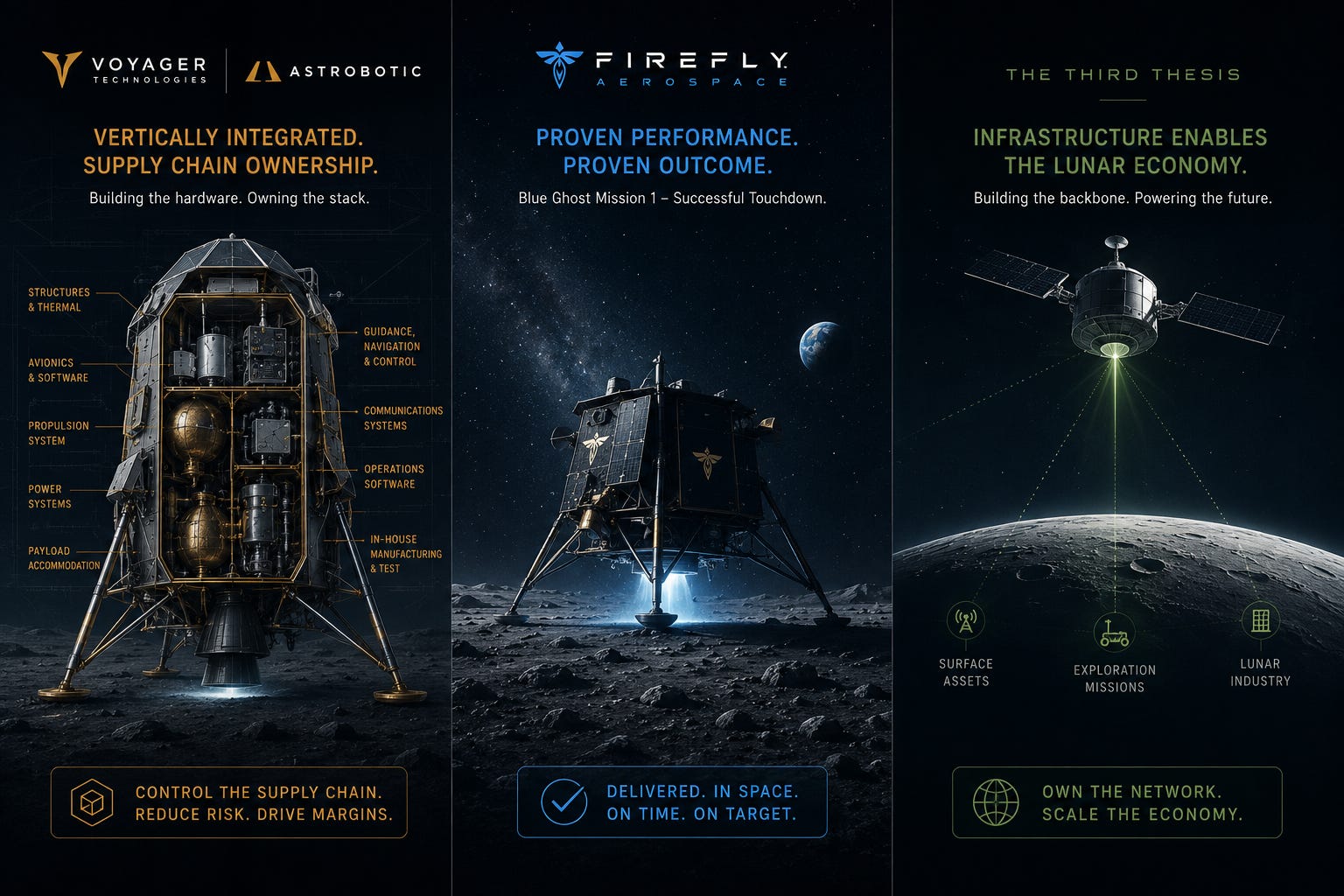

Lunar Delivery Is No Longer a Technology Problem

For most of the past decade, the central question in commercial lunar delivery was whether private companies could build spacecraft capable of reaching the Moon at all. That question now has at least a partial answer. Firefly Aerospace’s Blue Ghost Mission 1 landed softly on the lunar surface on March 2, 2025, completing a successful touchdown in Mare Crisium and operating for approximately 14 Earth days before the lunar night ended operations. It was the first fully successful commercial soft landing in history, Intuitive Machines’ IM-1 (Odysseus) had achieved a soft landing in February 2024 but tipped on its side, limiting surface operations, and it validated the basic proposition of NASA’s CLPS program: that fixed-price commercial contracts can deliver working spacecraft to the lunar surface for less than traditional cost-plus acquisition.

Astrobotic’s record is more complicated. Its Peregrine Mission One launched in January 2024 but suffered a propellant leak that prevented landing, with the spacecraft ultimately reentering Earth’s atmosphere. The company’s Griffin lander, designed to carry NASA’s Volatiles Investigating Polar Exploration Rover (VIPER) to the lunar south pole, continues development. The stakes for Griffin are high: CLPS contract continuity and the credibility of Astrobotic’s entire delivery roadmap depend on it executing cleanly.

The technology question, then, is no longer binary. It has fractured into a more interesting set of sub-questions: Who has the cost structure to survive between missions? Who has the revenue diversification to reduce NASA dependency? Who controls enough of their own supply chain to protect margin as production scales? The answers point in three different directions.

The Three Models

Voyager Technologies and the Vertical Integration Thesis

Voyager Technologies (NYSE: VOYG) went public in 2024 as a holding company for a portfolio of space and defense businesses. Its acquisition strategy has been deliberate: buy companies with specialized capabilities, integrate them into a broader service offering, and capture more of the value chain on any single government contract. The acquisition of Astrobotic, announced June 2, 2026, represents the most aggressive expression of that thesis.

Voyager’s stated rationale is acceleration. The company says it intends to scale Astrobotic’s lunar delivery and reusable rocket programs in support of NASA’s Moon Base architecture, which requires regular, affordable logistics runs to the lunar surface and eventually to a cislunar gateway. Voyager is effectively betting that lunar logistics will follow the same pattern as commercial resupply to the International Space Station (ISS): an early period of government-dominated demand, followed by a gradual opening of commercial payload opportunities, with the companies that built durable operational infrastructure during the government phase capturing the most valuable positions in the commercial phase.

The unit-economic logic of vertical integration is straightforward in theory. If Voyager can own spacecraft manufacturing, mission operations, and payload integration under one roof, it eliminates the sub-tier markups that currently inflate mission costs and retains margin that currently flows to suppliers. The risk is equally straightforward: vertical integration requires capital expenditure ahead of demand, and in a market where flight rates remain low, those fixed costs can be punishing.

Voyager reported total revenue of approximately $143 million for full-year 2024, with the substantial majority coming from government contracts. The Astrobotic acquisition adds a business with demonstrated CLPS contract relationships but also a mission failure on its record and a lander program, Griffin, that has not yet flown. The combined entity will carry meaningful integration risk in the near term, and the financial burden of maintaining Astrobotic’s development programs while absorbing the acquisition cost adds pressure to a balance sheet that investors should examine closely against NASA’s CLPS award cadence. What a 20% decline in CLPS task order cadence would mean for Voyager’s ability to fund Griffin through first flight is a scenario worth modeling before adding exposure.

The core decision question for investors evaluating Voyager: does the vertical integration premium materialize before the cash burn becomes structural?

"The next section maps how Astrobotic's CLPS dependency becomes Voyager's structural risk, then identifies the three variables that will determine which of these models reaches commercial self-sufficiency, and examines the theory of cislunar value accumulation that no current CLPS provider has fully committed to. Paid subscribers also receive five specific decision questions and related actions mapped to investor, supply chain executive, and teaming contexts, along with the full source and limitations disclosures behind every claim."