The Only Question That Matters Now for CLD Suppliers

The Architecture Changed, but the Risk Didn’t Go Away. It Moved.

Editors Note: Over the next two weeks, we will be presenting a series of articles about the recent changes in the Commercial LEO Destinations program and the effect those changes may have on the supply chain. This is the first of those articles.

What This Means

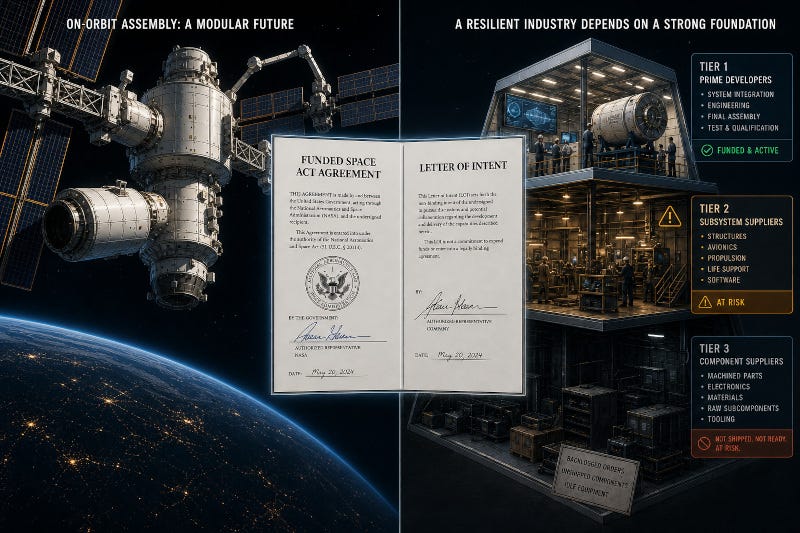

NASA’s March 2026 Ignition restructuring of Commercial LEO Destinations (CLD) is not just a policy story, it is a supplier exposure map waiting to be read. The pivot from certifying full commercial station operators to building a government-owned core module changes who gets paid, on what timeline, and under what contract vehicle. Tier 2 and Tier 3 suppliers who ramped capacity and signed teaming agreements based on expected Phase 2 awards are not created equal: their exposure depends almost entirely on whether they hold executed Funded Space Act Agreements (SAAs) or non-binding letters of intent (LOIs). Every supply chain leader with CLD exposure should know which one they have before the next procurement cycle opens.

There is a useful distinction, one that has not gotten nearly enough attention since March 24, 2026, between being stranded and being exposed.

Stranded means your capital is gone and your program is cancelled. Exposed means your capital is at risk and your program has changed shape. The second condition is more common right now, and more recoverable, but only if you understand precisely where you sit in the new architecture before the next round of procurement decisions.

NASA’s Ignition announcement restructured the Commercial LEO Destinations program in ways that every tier of the supply chain felt, but not in the same way. The agency formally shifted from certifying commercial operators to run complete station services, the original Phase 2 (full commercial station certification) ambition, toward a model in which NASA owns and operates a core module initially docked to the International Space Station (ISS), with commercial firms building add-on modules that attach to that core. The ISS is currently targeted for decommission in 2030, though NASA has historically extended ISS operational life under pressure. That clock gives this architecture both urgency and brittleness.

For the four active Commercial LEO Destination developers, Vast, Axiom Space, Starlab (the Airbus-Voyager joint venture), and Orbital Reef (Blue Origin and Sierra Space), the Ignition framework represents a forced strategy reset. But the downstream consequence that has received far less coverage is what it means for the supplier tiers below them.

The Two-Class Supplier Problem

The April 15, 2026 piece on this publication mapped the category of exposed suppliers. This analysis goes further: it names the structural mechanism that separates the most exposed firms from the merely disappointed ones.

The central dividing line is the contract vehicle. Firms that hold executed Funded Space Act Agreements for Phase 2 scope have a degree of financial protection, NASA has a documented obligation, and renegotiation at minimum creates a negotiating floor. Firms that accepted letters of intent, teaming agreement invitations, or verbal commitments from Phase 1 prime developers have no such floor. NASA has no binding obligation to those suppliers, and primes who issued teaming invitations ahead of Phase 2 awards have, in most cases, not executed binding subcontracts.

This creates two supplier classes with fundamentally different risk profiles operating under the same program umbrella. Both classes describe themselves as “CLD suppliers.” Only one has a legal instrument that matters.