What This Means:

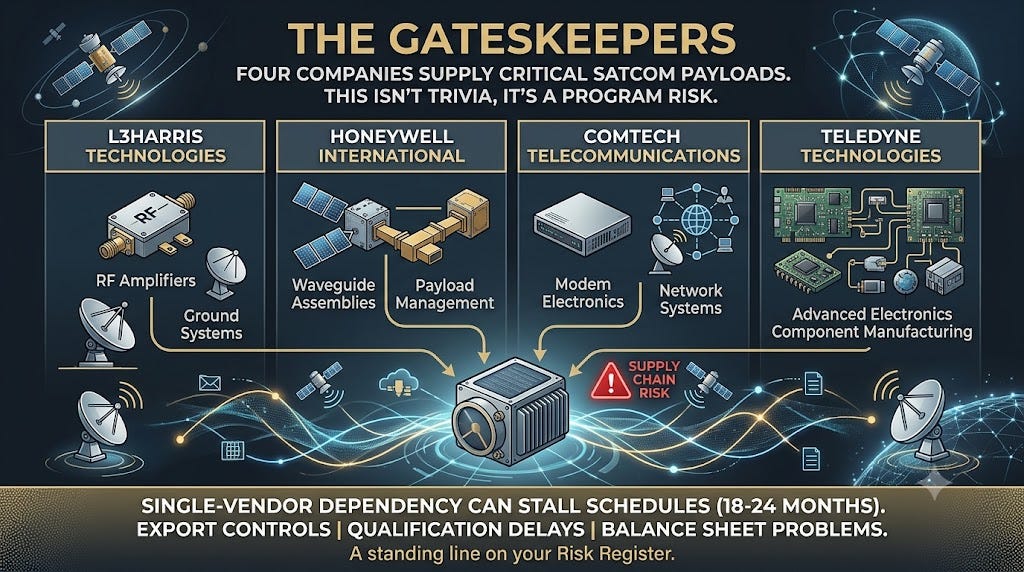

Four companies supply the radio frequency (RF) amplifiers, waveguide assemblies, ground terminals, and modem electronics that sit inside most military and commercial satellite communication payloads flying today. Those four are L3Harris Technologies, Honeywell International, Comtech Telecommunications, and Teledyne Technologies. That is not a trivia point, it is a program risk. A qualification delay, an export control action, or a balance sheet problem at any one of the four can stall payload schedules that already run 18 to 24 months from design freeze to flight unit. Executives and program managers building satellite communication payloads in the next two years should treat single-vendor dependency in this component tier as a standing line on their risk register, not a footnote discovered during a supplier audit.

If you run procurement for a satellite communication program, a version of this conversation has probably already happened in your building: a subsystem lead flags that the traveling wave tube amplifier (TWTA) vendor quoted a lead time of roughly 14 months instead of the 9 months assumed in last year’s proposal, illustrative numbers rather than a reported figure from any single program, and nobody on the team has a qualified second source ready to bid the replacement part. That conversation is becoming more common because the supplier base behind satellite communication hardware, unlike the launch vehicle market that gets most of the trade press attention, has quietly consolidated to a small number of qualified names.

This is not a story about a single contract or a single company stumbling. It is a story about structure. Four public companies, L3Harris Technologies (NYSE: LHX), Honeywell International (NASDAQ: HON), Comtech Telecommunications (NASDAQ: CMTC), and Teledyne Technologies (NYSE: TDY), hold overlapping and in several categories dominant positions across the RF front-end, amplifier, waveguide, and ground terminal component tiers that every satellite communication payload depends on. Whether you are a prime integrator deciding how to structure a bid, an investor assessing exposure to a thin supplier base, or a program manager trying to protect a schedule, the concentration in this tier deserves the same scrutiny that supply chain teams have already applied to launch vehicles and solid rocket motors.

The Signal: A Component Tier Nobody Maps the Way They Map Launch

Space supply chain coverage over the past two years has focused heavily on launch cadence, propulsion shortfalls, and structural materials such as titanium and carbon fiber composites. Far less attention has gone to the electronics tier that turns a satellite bus into a functioning communication payload. That is a gap, because the component categories inside a communication payload, the power amplifiers, RF switches, waveguide runs, modems, and ground terminal electronics, are qualified through processes that take longer to requalify than most structural parts. Once a prime integrator designs a payload around a specific traveling wave tube amplifier or a specific solid-state power amplifier line, switching vendors mid-program typically means re-running thermal vacuum qualification, radiation testing, and electromagnetic interference verification, a process that commonly runs 12 to 24 months depending on the part class, an industry-typical range rather than a figure tied to any single audited source.

Public company disclosures make the concentration visible without requiring a classified program office briefing. L3Harris Technologies, formed by the 2019 merger of L3 Technologies and Harris Corporation, reports satellite and airborne electronics through its Space and Airborne Systems segment and carries RF and microwave heritage from the former Harris Corporation antenna and communications business directly into current satellite terminal and payload component lines, as disclosed in the company’s Securities and Exchange Commission (SEC) Form 10-K filings. Honeywell International’s Aerospace Technologies segment supplies satellite communication terminals and avionics used in both commercial aviation connectivity and government satellite communication systems, and the company disclosed in a 2025 filing its plan to separate its Aerospace business into an independent, publicly traded company, a restructuring that will change the corporate reporting structure investors and procurement teams have used to track this supplier’s satellite communication exposure. Comtech Telecommunications, smaller by market capitalization than the other three, supplies satellite ground segment equipment, modems, and troposcatter systems, and has disclosed in recent SEC filings a series of debt covenant amendments and balance sheet restructuring steps that raise a distinct financial risk profile relative to its larger peers. Teledyne Technologies, through its Teledyne Defense Electronics and Teledyne e2v business units, supplies traveling wave tube amplifiers, RF and microwave components, and connectors used across both commercial and military satellite payloads, a position the company has expanded through acquisitions disclosed in its own SEC filings over the past several years.

None of these four companies is new to the space sector. What has changed is the degree to which program managers building new satellite communication constellations, particularly low Earth orbit constellations for the Department of Defense’s proliferated architecture programs, are discovering that the qualified vendor list for specific component categories is shorter than their proposal assumed.