The Elements China Controls

How Gallium and Germanium Export Restrictions Are Threading into the Space-Grade Solar Cell and GaN Supply Chain Right Now

What This Means

China’s export controls on gallium and germanium, formalized in August 2023 and tightened through 2024 and into 2025, are not an abstract geopolitical signal. They are a physical constraint on the raw material inputs that underpin space-grade solar cells, gallium nitride (GaN) radio frequency (RF) components, and silicon carbide (SiC) power electronics. China produces approximately 80% of the world’s refined gallium and 60% of its refined germanium. Every prime contractor building high-efficiency triple-junction solar arrays, every constellation operator procuring GaN-based amplifiers, and every program manager sourcing SiC power converters now sits downstream of a supply chain with a documented, government-imposed chokepoint at the top. The question is not whether this exposure exists. The question is whether your program has mapped it, priced it, and built around it before the next procurement cycle closes.

Two Elements, One Government, a Decade of Underinvestment

On July 3, 2023, China’s Ministry of Commerce announced that exporters would be required to obtain licenses for shipments of gallium and germanium compounds and related metals. The controls took effect August 1, 2023. China subsequently expanded the framework, adding antimony to the list in September 2024 and, in a significant escalation in December 2024, placing restrictions on gallium, germanium, indium, and other critical materials specifically in response to U.S. semiconductor export restrictions targeting advanced chips and chip-making equipment destined for China.

The December 2024 round closed the remaining policy ambiguity. Where the August 2023 controls left room for interpretation about scope and enforcement pace, the December 2024 restrictions cited U.S. semiconductor export controls as the explicit trigger and signaled that Beijing is prepared to use critical mineral supply as an instrument of technology policy for the long term.

For the space supply chain, the relevant exposure is not in finished satellites or launch vehicles. It concentrates three levels upstream, in the refined metal and compound semiconductor wafer production that feeds solar cell junctions, RF front-end modules, and power management electronics. Understanding that upstream map is the first step in assessing actual program risk.

The Supply Chain Map: Where Gallium and Germanium Actually Enter Space Hardware

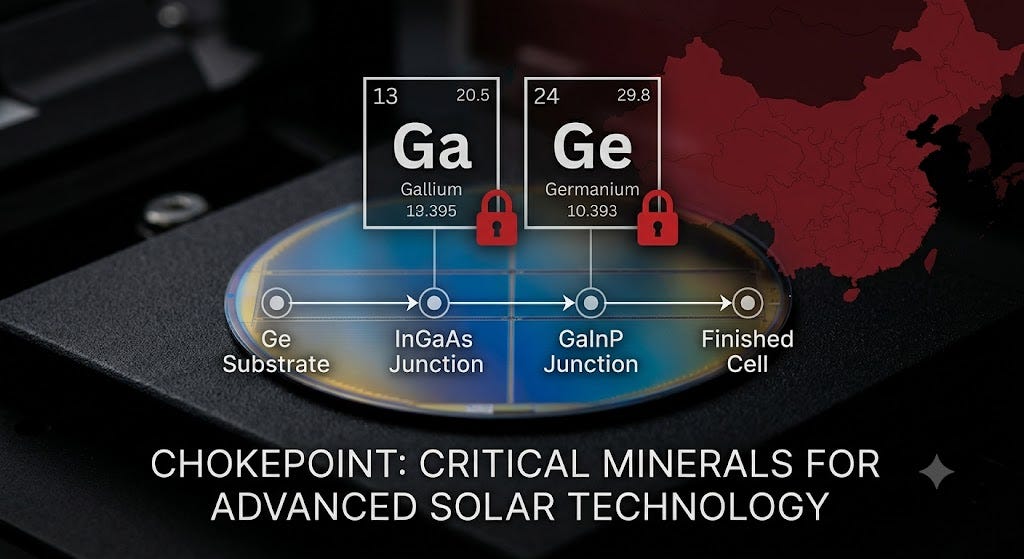

Solar Cells: Germanium as the Load-Bearing Substrate

Space-grade solar cells are not silicon. The photovoltaic devices used on commercial satellites, government spacecraft, and deep-space probes are triple-junction cells built on a germanium (Ge) substrate. The germanium wafer is the mechanical and electrical foundation of the cell. Germanium is chosen because its lattice constant closely matches the indium gallium arsenide (InGaAs) and gallium indium phosphide (GaInP) junctions grown on top of it, enabling the cell to capture a broader spectrum of sunlight at efficiencies that routinely exceed 30%.

The three primary manufacturers of space-grade triple-junction solar cells serving the Western market are Spectrolab, a subsidiary of Boeing; SolAero Technologies, acquired by Rocket Lab in January 2022; and Azur Space Solar Power, a German firm. Based on U.S. Geological Survey (USGS) production share data and industry-wide sourcing patterns documented in Class 2 trade sources, all three are likely exposed to Chinese-origin germanium at the substrate level; however, individual company sourcing has not been confirmed through Class 1 disclosure. Umicore, the Belgian materials company, is the leading non-Chinese processor of germanium, but Umicore sources germanium concentrate from zinc smelting byproduct streams, and the geographic concentration of that supply remains a partial offset rather than a complete alternative.

The USGS documented in its 2024 Mineral Commodity Summaries that the United States has no domestic primary germanium production. All U.S. germanium supply is either imported or recovered from secondary sources. China’s share of global germanium production is cited by the USGS at approximately 60%, with Germany and Belgium accounting for meaningful but substantially smaller secondary processing capacity.

For program managers, the practical consequence is this: a satellite solar array that appears to be domestically sourced at the cell and panel level may nonetheless carry full Chinese germanium exposure at the substrate level. That substrate-level exposure does not appear in most standard supply chain audits because the audit boundary stops at the Tier-2 cell manufacturer, not the Tier-3 or Tier-4 material input.

The next sections map exactly where gallium enters the GaN RF supply chain, which specific manufacturers carry unhedged input exposure, why the December 2024 indium restrictions compound the solar cell risk, and what the 12-to-24-month qualification barrier means for programs in production right now. Paid subscribers also receive the five specific procurement actions, with named alternative suppliers and the contractual questions your legal team needs to address before the next cycle closes. This is the tier-by-tier map that standard supplier questionnaires do not reach.