What This Means

SpaceX’s June 2026 initial public offering (IPO) was the largest in stock market history, but the prospectus told investors almost nothing about the supplier relationships that keep Starship launching, Starlink scaling, and Dragon flying. Beneath SpaceX’s celebrated vertical integration sits a web of single-source dependencies, sanctioned-country material flows, and constrained specialty suppliers that the public market has not yet fully priced into its risk models. Supply-chain leaders, program managers, and executives whose programs compete for the same Tier-2 and Tier-3 capacity as SpaceX now face a materially changed sourcing environment, one where the world’s most capitalized launch customer sits at the front of every allocation queue.

The IPO Changed the Information Environment

When SpaceX priced shares on June 11, 2026, listed on Nasdaq under the ticker SPCX, and closed its debut at $161, up 19 percent on the first day and another 20 percent on the second, the company did not simply hand investors a piece of the commercial space economy. It handed analysts, competitors, procurement officers, and supply-chain managers a reason to map every sub-tier relationship SpaceX depends on. (Pricing details reflect the SEC EDGAR registration statement and prospectus supplement filed in connection with the offering.)

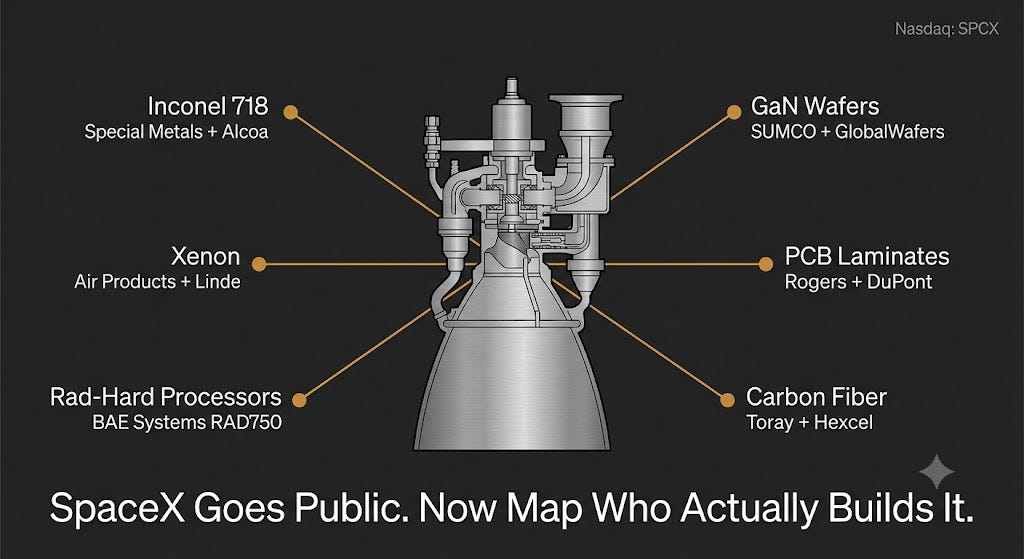

Until the IPO, SpaceX’s supplier network was largely opaque. The company filed no public financial disclosures, disclosed no program-level procurement data, and cultivated a reputation for vertical integration so thorough that the supply chain question seemed almost moot. The prospectus changed that perception without actually resolving it. SpaceX’s Washington State facility produces solar array elements, Ka-band antennas, and payload channel components in-house. Its Hawthorne, California campus machines Merlin and Raptor engine components under the same roof that assembles Dragon capsules. But “in-house” is not “from scratch.” Every gram of Inconel 718 in a Raptor combustion chamber arrived from somewhere. Every radiation-hardened processor in a Starlink satellite was fabbed at a node SpaceX does not own. Every kilogram of xenon loaded into a Hall-effect thruster was refined by one of three suppliers on the planet.

The IPO made SpaceX a public company. It did not make its supply chain less concentrated.

The Signal: Three Programs, Three Exposure Profiles

Starship, Starlink, and Dragon each carry distinct supply-chain risk profiles. Mapping them together reveals not redundancy but compounding exposure, cases where a constraint on one program’s material or component supply directly pressures another program’s production cadence and, by extension, the broader commercial and government customers competing for the same supplier capacity.

Starship: Superalloys, Propellants, and Structural Steel

Starship’s Raptor 3 engine burns liquid methane and liquid oxygen in a full-flow staged combustion cycle that achieves combustion chamber pressures above 300 bar. That pressure regime requires materials that commercial aviation never demands at comparable volumes.

Inconel 718 is the primary structural alloy in the turbopump and hot-gas manifold sections. Current lead times from qualified aerospace-grade producers sit at 28 to 32 weeks, based on supply-chain tracking compiled in the Ex Terra Media Space Commerce Supply Chain Consolidated Reference File (a JOSC-originated inference from distributor-level data, not an independently published figure). Three suppliers dominate the qualified production base: Alcoa Corporation, which processes the alloy at its Davenport, Iowa facility; Special Metals Corporation (a subsidiary of Precision Castparts), the original developer of the alloy and still the dominant certification-holder for critical aerospace applications; and VSMPO-AVISMA, the Russian-state-affiliated producer that is the world’s largest supplier of aerospace-grade titanium alloys and also produces some nickel-based superalloys, and whose post-2022 Western sanctions exposure has created qualification gaps that U.S. and European primes have not fully closed across both titanium and superalloy supply chains.

SpaceX has not publicly disclosed its current Inconel 718 sourcing mix. The VSMPO-AVISMA exposure is, in the titanium and related specialty-alloy chain, a supply-chain-wide problem: any prime or sub-tier supplier that relied on Russian material certifications before 2022 is still working through requalification with Western mills. That requalification process runs 12 to 24 months per alloy grade per application, and the backlog at Special Metals and at Alcoa’s aerospace-grade production lines is directly connected to that post-sanction demand surge. Programs competing with SpaceX’s Starship production rate for Inconel 718 allocation are competing with the most capitalized customer in the sector.

Stainless steel (specifically 301 full hard) is Starship’s primary structural skin material, a deliberate design choice by SpaceX that departed from aluminum-lithium composites. The shift simplified fabrication but created demand at a different supplier tier: heavy-gauge aerospace stainless steel rolling, precision ring rolling for the forward skirt and interstage sections, and friction-stir welding of large-diameter rings all require specialized equipment that is not commodity-available. The tank dome sections are sourced from a small number of U.S. and European precision-forming shops with the required diameter capacity. None of these shops are publicly identified in SpaceX’s filings.

Liquid methane and liquid oxygen are produced at or near the Boca Chica, Texas launch site. The propellant supply chain is relatively deconcentrated for methane but tightens on liquid oxygen at the production-purity grade required for full-flow staged combustion. Industrial gas suppliers Air Products and Chemicals, Inc., Linde plc (which acquired Praxair in 2018 and has integrated the legacy Praxair production infrastructure), and regional industrial gas producers serve the U.S. market. At cryogenic purity grades for propulsion applications, the qualified supplier list narrows further. No public Class 1 disclosure names SpaceX’s specific propellant contract arrangements.

The next sections map Starlink's radiation-hardened electronics exposure, the three-supplier xenon market, Dragon's parachute and thermal protection single-source concentrations, and the three cross-program nodes that carry compounding risk across all three SpaceX programs simultaneously. Paid subscribers also receive the five specific procurement actions supply-chain leaders should execute now, plus the full decision framework for investors with exposure to the named sub-tier suppliers.