Space Semiconductors Market Insights 2025

Annual Growth Projected to be More Than Eight Percent

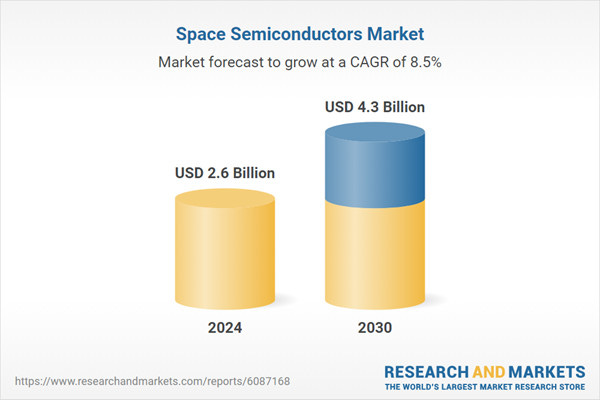

The global market for Space Semiconductors was valued at $2.6 billion in 2024 and is projected to reach $4.3 billion by 2030, growing at a CAGR of 8.5% from 2024 to 2030, according to a new report from Global Industry Analysts, Inc.

This comprehensive report provides an in-depth analysis of market trends, drivers, and forecasts, helping you make informed business decisions, and includes the most recent global tariff developments and how they impact the Space Semiconductors market.

Space semiconductors are specially designed electronic components engineered to operate reliably in the harsh and unpredictable conditions of space. Unlike commercial-grade chips, space-qualified semiconductors must withstand extreme temperatures, vacuum exposure, radiation, and electromagnetic interference. These chips are foundational to satellite systems, spacecraft avionics, deep-space probes, and interplanetary rovers, enabling core functions such as signal processing, data transmission, power regulation, and attitude control.

Radiation-hardened (rad-hard) and radiation-tolerant semiconductors are particularly vital for space missions, where exposure to cosmic rays and solar flares can degrade or destroy conventional electronic components. As satellite and exploration payloads become more advanced and data-intensive, the demand for high-performance computing and secure communication hardware is intensifying. Space semiconductors form the brain of onboard systems, making their reliability critical to mission success, longevity, and safety.

Satellite communications is the dominant application segment, with rising demand from commercial broadband constellations, military satellites, and Earth observation platforms. Navigation, telemetry, and environmental monitoring systems also rely heavily on space semiconductors. Defense and intelligence agencies are increasing investments in secure, radiation-hardened processors to enhance situational awareness and satellite command resilience. The trend toward autonomous spacecraft, robotic landers, and lunar habitats is opening new frontiers for high-reliability, low-latency semiconductor devices.

North America leads the global space semiconductor market due to the dominance of U.S. defense contractors, satellite OEMs, and government space programs like NASA and the Department of Defense. Europe is expanding capabilities through ESA and national initiatives in secure satellite infrastructure. Asia-Pacific is rapidly growing, led by China, India, and Japan, where domestic launch capabilities and indigenous satellite production are accelerating semiconductor procurement. International collaboration in satellite development - especially through joint Earth observation and telecommunication missions - is further boosting cross-border demand for space-qualified chips.

The market is driven by the growing number of satellite launches, increasing complexity of space missions, and the demand for fault-tolerant electronics in harsh environments. The shift from large, geostationary satellites to smaller, distributed constellations requires a new generation of semiconductors that balance performance, radiation resistance, and miniaturization. Advances in materials like GaN, SiC, and SOI, along with RHBD methodologies, are enabling reliable chip design for space deployment.

Expanding commercial participation in satellite broadband, Earth analytics, and deep-space exploration is creating robust demand across civil, commercial, and defense segments. The strategic importance of domestic semiconductor manufacturing for national security, coupled with supportive space policies and investments in secure, sovereign supply chains, is further propelling market growth. As space platforms become more intelligent, autonomous, and interconnected, semiconductors will remain a linchpin in powering and protecting mission-critical operations in orbit and beyond.