Space Semiconductor Market to Reach $4.8 Billion by 2032

Satellite Communications, EO Driving Market Growth

Space semiconductors include the increasing demand for satellite communication and Earth observation, advancements in satellite technology, the rise of satellite constellations, expanding space exploration initiatives, and the need for reliable and radiation-hardened components in space missions. Furthermore, the growing need for global connectivity, internet access, and data transmission drives the demand for satellite communication systems. Additionally, the rise in Earth observation applications for purposes such as weather monitoring, disaster management, agriculture, and urban planning contribute to the demand for space-based sensors and imaging systems, which rely on semiconductor components for data processing and transmission.

According to a new report from Allied Market Research, the space semiconductor industry size generated $2.1 billion in 2022 and is anticipated to generate $4.8 billion by 2032, witnessing a CAGR of 8.8% from 2023 to 2032.

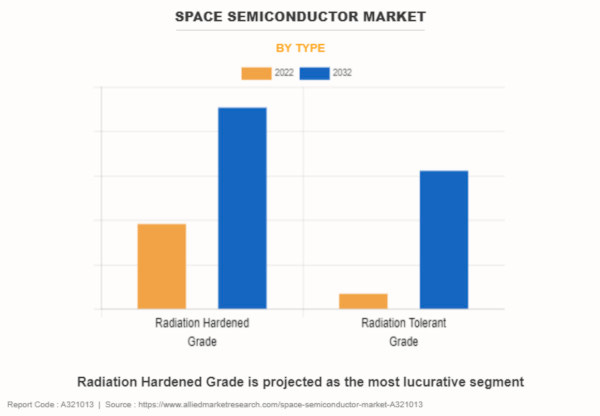

On the basis of type, the radiation hardened grade segment held the highest market share in 2022, accounting for more than two-thirds of the global space semiconductor market revenue. This is attributed to the fact that radiation hardened grade semiconductor components are specifically designed and manufactured to withstand the harsh radiation environment present in space. Given that space missions expose electronic systems to various forms of radiation, including cosmic rays and solar radiation, radiation hardened grade components are essential for ensuring the reliability and longevity of these systems.

However, the radiation tolerant grade segment is projected to manifest the fastest CAGR of 12.2% from 2023 to 2032. This is attributed to the fact that radiation-tolerant components offer a balance between radiation resilience and cost-effectiveness, making them suitable for a wide range of space missions with varying requirements. Semiconductor manufacturers can develop radiation-tolerant components that meet the specific needs of different missions, providing flexibility and versatility to space system designers.

On the basis of component, the integrated circuits segment held the highest market share in 2022, accounting for around one-third of the global space semiconductor market revenue. This is attributed to the fact that integrated circuits offer high performance and efficiency, making them well-suited for space applications where reliability and functionality are paramount. Semiconductor manufacturers are continually improving the performance of ICs, including higher processing speeds, lower power consumption, and increased functionality, which are critical for meeting the demanding requirements of space missions.

However, the sensors segment is projected to manifest the fastest CAGR of 13.5% from 2023 to 2032. This is attributed to the fact that space missions require a wide variety of sensors to meet different operational needs. These include temperature sensors, pressure sensors, inertial sensors (such as accelerometers and gyroscopes), radiation sensors, imaging sensors, and more. Each sensor type serves specific purposes in different phases of a mission, from launch and orbit to landing or reentry.

On the basis of application, the satellite segment held the highest market share in 2022, accounting for more than one-third of the global space semiconductor market revenue and is estimated to maintain its leadership status throughout the forecast period. This is attributed to the fact that satellites are essential components of modern communication, navigation, Earth observation, and scientific research networks. They serve as critical infrastructure for a wide range of applications, including telecommunications, broadcasting, weather forecasting, navigation, surveillance, and disaster management.

Semiconductor components are fundamental to the operation of satellites, driving the demand for space-grade semiconductors. However, the launch vehicles segment is projected to manifest the fastest CAGR of 10.0% from 2023 to 2032. This is due to the fact that launch vehicle manufacturers are continuously striving to reduce the size, weight, and power consumption of onboard electronics to increase payload capacity and improve overall efficiency. This trend drives the demand for compact, lightweight, and energy-efficient semiconductor components, including microcontrollers, sensors, communication modules, and power management ICs.

On the basis of region, North America held the highest market share in terms of revenue in 2022, accounting for more than one-third of the global space semiconductor market revenue. This is attributed to the fact that the U.S. is a global leader in semiconductor technology and innovation, with a robust ecosystem of semiconductor manufacturers, research institutions, and technology companies.