Space Launch Services Market Revenue May Reach $57.94 Billion by 2033

Multiple Factors Fueling Rapid Growth, Report Says

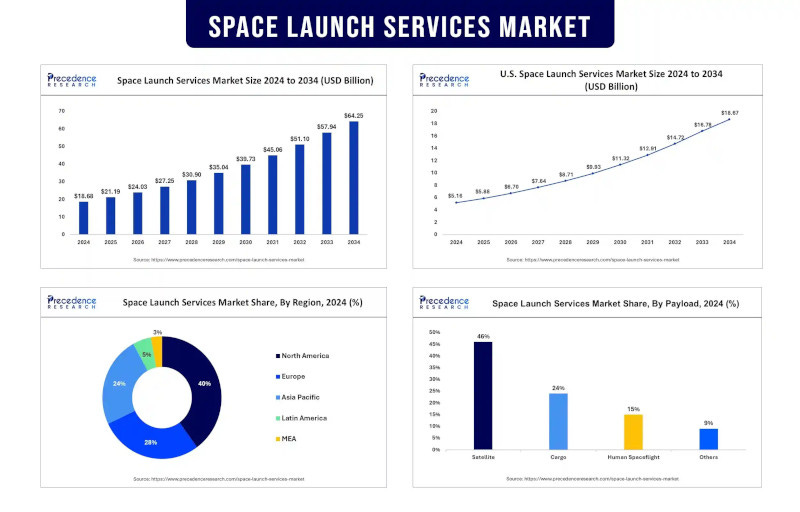

The space launch services market revenue reached $21.19 billion in 2025 and is predicted to attain around $57.94 billion by 2033 with a CAGR of 13.15%, according to a new report from Precedence Research. The market is witnessing rapid growth due to increasing demand for satellite deployment, expansion of commercial space enterprises, and heightened investment in reusable launch vehicles.

The space launch services industry is gaining momentum as satellite-based technologies, space exploration, and defense modernization continue to evolve. With the growing need for broadband connectivity, Earth observation, and global navigation, satellite launches are in high demand. Changes in the space industry are being brought on by more public-private partnerships, new advances in rocket technology, and the switch to reusing rockets.

The report from the Satellite Industry Association (SIA) for 2024 stated that over 85% of all launches last year were for communication, imaging, and internet services. Reusable rockets, led by pioneers including SpaceX, have significantly reduced launch costs, democratizing space access for smaller enterprises and emerging nations. The development of spaceports in various regions is also enhancing market accessibility and operational capacity.

The transition from expendable to reusable rockets is revolutionizing the economics of space launches. The flights of SpaceX’s Falcon 9 and Falcon Heavy, Blue Origin’s New Shepard and expected systems from Rocket Lab and ISRO are preparing for affordable and environmentally friendly space transportation. The FAA found that, as of 2024, more than 60% of all orbital launches involved some reusable technology. While depending on traditional big boosters, NASA’s Artemis program has chosen SpaceX’s Starship for future cargo missions to the Moon. SpaceX reached a new milestone in 2024 by flying the same Falcon 9 first stage for the 20th time. The European Space Agency (ESA) started Themis to test reusable stages that are part of its next generation of launch vehicles. Furthermore, these innovations greatly cut down on the time needed for a flight, raise the number of flights and draw new players to the space industry, thus facilitating the space launch service industry growth.

Mega-constellation projects such as Starlink, OneWeb, and Amazon’s Project Kuiper are key drivers of market demand. As per the Satellite Industry Association (SIA), 4,562 LEO satellites were launched in 2024, and it predicts that by 2030 there will be as many as 50,000. Their presence supports broadband access worldwide, remote sensing and IoT applications. The high demand leads to frequent launches, with most being rideshare or launches dedicated to small satellites.

Spacefaring nations continue investing heavily in launch services via partnerships with private entities. Nations active in space travel are still spending big on launch services by partnering with private companies. Space industries, such as NASA, ESA, ISRO, and CNSA, turn to commercial space companies for their orbital deliveries, which helps lower costs. SpaceX, ULA, and Blue Origin were all awarded contracts by NASA in 2024 as part of the CLPS initiative, which helped create competition in the field.

Global investments in launch infrastructure are accelerating. Countries like the UK, India, Australia, and Brazil are developing new spaceports to support vertical and horizontal launches. In 2024, ISRO inaugurated the second commercial spaceport in Kulasekarapattinam, Tamil Nadu to handle the rising launch demand and reduce overcrowding at Sriharikota. The UK Space Agency helped develop SaxaVord Spaceport, and in 2024, it performed its inaugural suborbital mission, intended to bring orbital missions to life by 2025. The goal is to move beyond high-profile sites and ensure that more people and space programs everywhere access space launch services, avoid delays, and add more stakeholders to the global space field.