Space Debris Removal Market Worth $600 Million by 2028

CAGR Estimated to be 41.7 Percent Over the Next Five Years

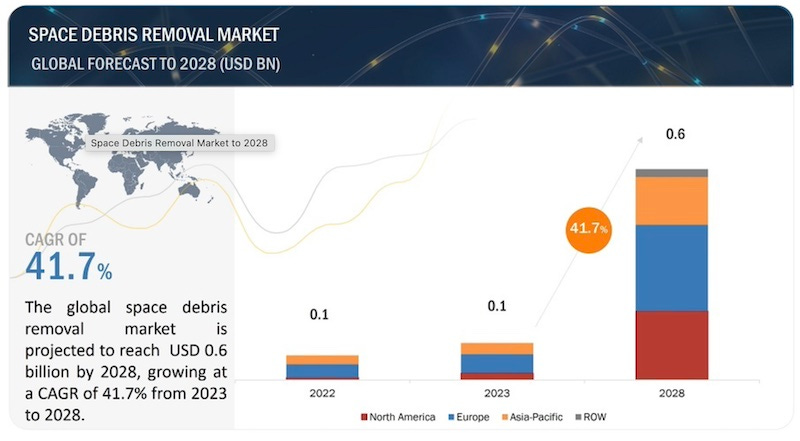

The Space Debris Removal market is valued at $100 million in 2023 and is projected to reach $600 million by 2028, at a CAGR of 41.7% from 2023 to 2028 according to a new report by MarketsandMarkets. The space debris removal market is a subset of the satellite and technology industry that focuses on the development and deployment of space debris removal solutions and services.

Space debris removal refers to the strategic process of eliminating defunct satellites, spent rocket stages, and fragments from space orbit. This burgeoning industry aims to mitigate orbital congestion, safeguard operational satellites, and ensure sustainable space exploration. By deploying innovative technologies and retrieval strategies, companies engage in the retrieval, capture, and disposal of space debris, fostering a cleaner orbital environment for continued commercial satellite launches and enhancing the long-term viability of space activities.

The direct debris removal segment is estimated to lead the space debris removal market from 2023 to 2028. Direct debris removal involves the capture and active removal of orbital debris from space. The rise of direct debris removal techniques is due to the urgent need for clearing space clutter. The growing number of satellites and spacecraft in orbit increases the likelihood of collisions with debris, highlighting the need for effective removal strategies. Additionally, technological advancements in robotic arms, nets, and other capture mechanisms, as well as improvements in propulsion and rendezvous techniques, are making direct debris removal increasingly feasible.

The LEO segment is projected to grow at the highest CAGR. LEO orbit satellites provide stable, continuous coverage, making them vital for services such as broadband internet, telecommunication, and broadcasting. The demand for real-time data and global connectivity further underscores their significance. The growing debris density in this belt has triggered the need to clear space junk in order to maintain the safety of operational satellites. Technological advancements and cost-effective deployment methods are also contributing to removing debris from this orbit.

The multiple technique segment in the space debris removal industry is primarily driven by the need to have multiple techniques in order to remove debris of different sizes. Combining different techniques can lead to synergistic effects, enhancing the overall effectiveness and efficiency of debris removal missions. A single technique may not be effective for all types of debris, making a multiple-technique approach necessary to address the entire debris population. These factors collectively propel the growth of the multiple technique segment, addressing evolving business and mission requirements.

The commercial end user segment in space debris removal is primarily driven by the critical need to protect satellite assets. Satellite operators, telecommunication companies, and Earth observation firms heavily rely on space infrastructure for their operations. With the rise in satellite constellations and increasing dependency on space-based services, safeguarding these assets against potential collisions with space debris is paramount. Mitigating the risk of damage or loss of satellites ensures uninterrupted services and protects substantial investments. Hence, commercial entities are actively seeking efficient space debris removal solutions to secure their space assets and maintain operational continuity.

North America is home to some of the biggest players in the space debris removal market, including Northrop Grumman, and Kall Morris Incorporated. These companies have a wealth of experience and expertise in space technology, and they are investing heavily in the development of space debris removal systems. The North American government is a major supporter of the space industry. The government has invested millions of dollars in research and development of this technology, and it is also providing funding for the deployment of orbital debris removal solutions.

Space debris removal is dominated by a few globally established players such as Astroscale (Japan), ClearSpace (Switzerland), Surrey Satellite Technology Ltd (UK), Northrop Grumman (US), and Kall Morris Incorporated (US).