Sierra Space’s Zero-Touch Solar Array Line Is a Cost Signal Legacy Suppliers Can’t Ignore

What This Means:

Sierra Space’s move to automate solar array production using surface-mount technology (SMT) assembly methods borrowed from electronics manufacturing is not a factory upgrade story. It is a cost-structure signal. If zero-touch production strips out the labor-intensive steps that have defined solar array economics for three decades, incumbents who still hand-build arrays face a margin and market-share test. That group includes Boeing’s Spectrolab cell business and Redwire Corporation’s Roll-Out Solar Array line, just as constellation-scale demand accelerates. Investors tracking Redwire (NYSE: RDW) and other publicly exposed power-system names, along with executives at legacy suppliers deciding whether to automate now or compete on the old cost curve, should treat this as the moment to reassess unit economics before the next high-volume constellation award locks in a winner.

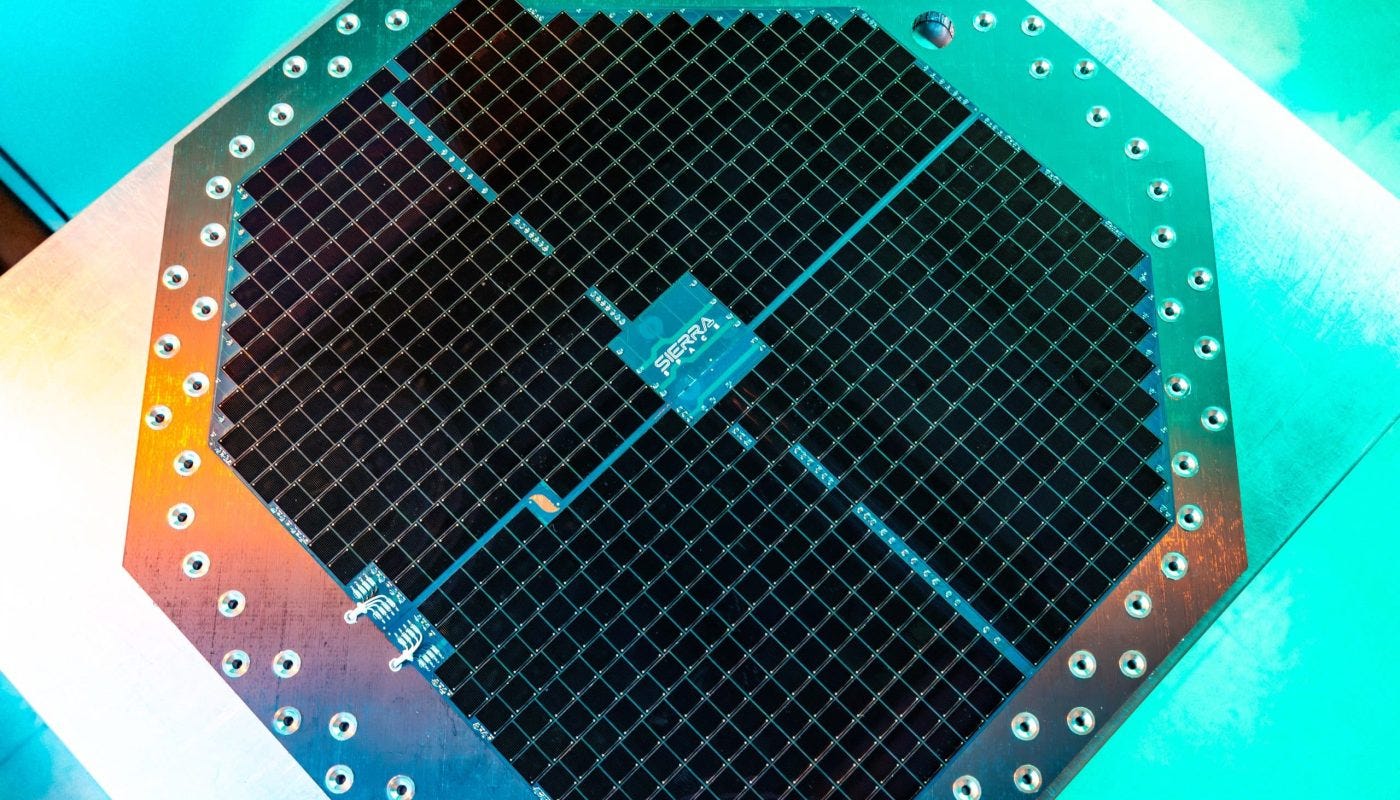

Sierra Space has told the market it can build solar arrays with a production process that removes most of the manual touch labor traditionally required for cell stringing, panel lamination, and harness integration. The company describes the approach as “zero-touch” automated manufacturing, applying surface-mount technology (SMT), the same automated placement and soldering discipline used to assemble printed circuit boards, to a product category that has historically been built by hand in small batches at aerospace-grade tolerances.

That distinction matters more than the press release language suggests. Solar array production has resisted automation for reasons that are structural, not incidental: cell strings are fragile, panel substrates vary by mission, and qualification testing has traditionally assumed a build process with a human inspector at every joint. A manufacturer that can automate cell placement and panel assembly at scale is not making arrays faster for its own missions. It is changing what a competitive bid looks like for every buyer who currently pays a hand-assembly premium, whether that buyer is the National Aeronautics and Space Administration (NASA), a defense prime, or a commercial constellation operator sourcing thousands of units.

The signal here is directional, not definitive. Sierra Space has not published unit-level cost data, and no Class 1 filing quantifies the labor-hour reduction the automated line achieves. That announcement dates to September 2023, and no Class 1 source through the research cutoff confirms a subsequent contract award or qualification milestone, a gap addressed further in the Limitations section below. What is verifiable is the strategic intent: Sierra Space has publicly stated its automated line is intended to support both its own Dream Chaser spaceplane and Large Integrated Flexible Environment (LIFE) inflatable habitat programs and to serve as a production capability the company can offer to external customers through its Space Systems division, the unit that traces its manufacturing heritage to Sierra Nevada Corporation’s decades of solar array and power system work on NASA and Department of Defense (DoD) missions including GPS III, Mars 2020, MAVEN, and Tracking and Data Relay Satellite (TDRS) spacecraft.

That heritage is the part of the story investors should not skip past. Sierra Space is not a startup trying to break into solar arrays from nothing. It already has flight heritage, government customer relationships, and a qualified supply base. Layering automated production onto that base is a different competitive threat than a new entrant with no track record trying to win its first contract. It is an established supplier trying to win on cost against other established suppliers.

Data Foundation

The Class 1 basis for this signal is narrower than the narrative around it, and that gap should shape how aggressively investors and executives act on it.

Sierra Space’s own public statements describing the automated, SMT-based solar array line function as a Class 1 source for the fact that the company built and announced the capability, and for the stated intent to apply it across Dream Chaser, LIFE habitat, and third-party production. Company-issued releases carry Class 1 weight for what the company says it did; they do not carry the same weight for sector-wide cost or throughput comparisons, since the company has an incentive to characterize its own capability favorably. Any claim about how much cheaper or faster the automated line is relative to competitors should be read as a company assertion, not an audited fact, until an independent source confirms it.

On the legacy-supplier side, Redwire Corporation is the cleanest publicly traded proxy for this signal because it is a Securities and Exchange Commission (SEC) registrant. Redwire’s SEC filings identify its Roll-Out Solar Array (ROSA) product line, the flexible, deployable array technology used on the International Space Station power upgrade, NASA’s Gateway program, and multiple national security payloads, as part of its space infrastructure business. Those filings do not break out ROSA unit production costs or labor-hour figures, which means the market currently has no direct, apples-to-apples Class 1 comparison between Redwire’s build process and Sierra Space’s automated line. That is a real Class 1 Gap, flagged here rather than papered over with an inferred cost differential.

Boeing’s Spectrolab subsidiary, the dominant supplier of space-qualified solar cells used across most Western commercial and government missions, presents the same limitation in a more acute form. Spectrolab’s financials are folded into Boeing’s broader Defense, Space and Security segment reporting and are not separately disclosed, so there is no Class 1 figure available for Spectrolab-specific cost structure or capacity. Any claim about Spectrolab’s exposure to an automation threat is, by necessity, an inference based on its position as a manual-process incumbent in a segment now facing an automated entrant, not a documented fact.

One comparable data point does carry stronger Class 1 support: SpaceX’s own manufacturing approach for Starlink. SpaceX has stated, and space trade press has consistently reported, that it manufactures Starlink’s solar arrays and other satellite components in-house at its Redmond, Washington facility rather than sourcing them from third-party array suppliers, a vertical integration decision widely credited with helping the company hit unit-cost and production-rate targets that traditional aerospace supply chains have struggled to match. This is not a new phenomenon Sierra Space invented. It is a pattern SpaceX already validated at fleet scale, and Sierra Space’s automation move extends that pattern into a form other operators, who do not want to build their own factory, could potentially buy as a service.