Satellite Solar Cell Materials Market Worth $96 million by 2030

Multiple Factors Driving Growth Forecast

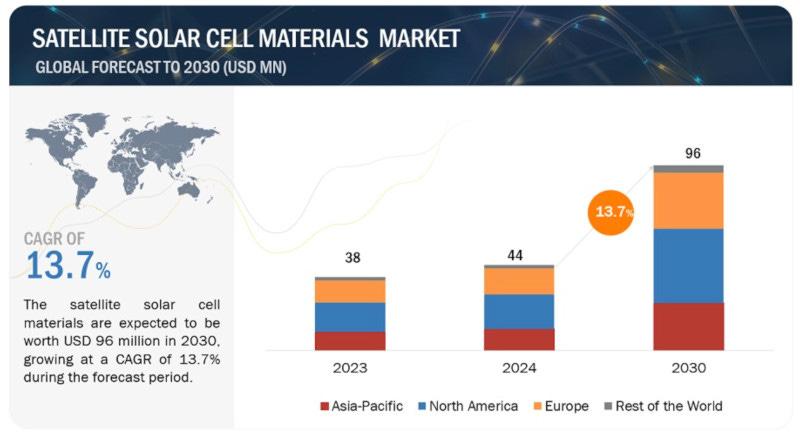

The Satellite Solar Cell Materials Market is expected to reach $96 million by 2030, up from $44 million in 2024 and grow at a CAGR of 13.7%, according to a new report from MarketsandMarkets.

Solar cells are important for powering a variety of space missions. While silicon remains the industry leader due to its low cost and known technology, advances in materials such as GaAs, Germanium multi-junction cells promise improved efficiency and radiation resistance. The market meets the diverse requirements of different satellites, ranging from low-cost options for cube satellites to high-performance materials for deep space research. However, issues such as high material costs and the need to balance efficiency, cost, and durability persist. As R&D efforts continue, the future of the satellite solar cell materials market is bright, with advancements in materials science and technology holding the key to unlocking its full potential and powering the next generation of space exploration.

Satellite applications have the biggest market share in the satellite solar cell materials industry, which is driven by several major factors. To begin, satellites serve an important role in a variety of industries and sectors, including communication, navigation, remote sensing, weather forecasting, and scientific research. The widespread use of satellite-based services in various industries generates a considerable and ongoing need for solar cells to power these satellites. Second, advances in satellite technology, such as miniaturization, improved propulsion systems, and constellation development, have increased the scope and capability of satellite applications. This development demands dependable and efficient power generating technologies, with solar cells being the favored option because of their appropriateness for long-term missions. The plans to generate solar energy in space for use on Earth through satellites align with the increasing importance of satellites as the largest application in the solar cells market. In the context of generating solar energy in space for Earth, the use of satellites equipped with advanced solar cells showcases the versatility and innovation in space technology. This aligns with the broader trend of harnessing space-based resources for sustainable solutions on Earth. Furthermore, rising demand for satellite-based internet services, earth observation data, and real-time worldwide connectivity is increasing the market share of satellite applications in the satellite solar cell materials market. Overall, the combination of critical roles across multiple industries, technological breakthroughs, environmental concerns, and rising market prospects reinforces satellite applications' supremacy in driving demand for solar cell materials.

Polar orbits have the biggest market share in the satellite solar cell materials market due to a variety of reasons that contribute to their popularity and demand. For starters, satellites in polar orbit provide enormous global coverage, making them critical for applications such as Earth observation, environmental monitoring, and reconnaissance that need extensive spatial data collection. Polar orbits provide unique orbital properties that allow satellites to travel over nearly every point on the planet's surface, allowing for a wide range of applications. Additionally, polar orbit satellites are frequently deployed for scientific research missions, space exploration endeavors, and multinational collaborations, necessitating the use of dependable and efficient solar cells to power these projects.

Silicon material segments have the biggest market share in the satellite solar cell materials market due to numerous key aspects that support their dominance. For starters, silicon-based solar cells have a long history of durability and performance in space, making them an excellent choice for satellite applications. Silicon solar cells have great efficiency, outstanding radiation resistance, and have been demonstrated to be durable, all of which are required for long-term missions in harsh space environments. Furthermore, silicon is readily available and benefits from proven manufacturing methods, allowing for economies of scale and cost-effective manufacture. Furthermore, continuing developments in silicon solar cell technology have increased their efficiency and dependability, cementing their status as the preferred material for satellite power generation. Furthermore, silicon is compatible with existing satellite designs and equipment, which ensures seamless integration and reduces deployment costs, making it a practical choice for satellite manufacturers. Another important aspect contributing to silicon's dominance is its adaptability, which allows it to match specific performance requirements and suit fluctuating mission needs. While other materials like Gallium Arsenide (GaAs) provide higher efficiency, silicon's balance of performance, dependability, and cost-effectiveness keeps it the favored material type for a wide range of satellite applications. Overall, the combination of dependability, performance, scalability, and versatility places silicon material segments as the largest and most dominating segment in the satellite solar cell materials market, acting as the foundation of solar power generation for satellites in orbit.

Asia Pacific is forecast to be the fastest-growing area in the satellite solar cell materials market, due to several key reasons that are driving its quick rise. Specifically, the region is experiencing a rise in economic development and scientific innovation, resulting in greater investments in space research and satellite technologies. Countries such as China, India, and Japan are leading the way with ambitious space programs, creating a significant need for solar cell materials to power satellite deployments.