Satellite Propulsion Market Projected to More Than Double by 2031

Electric Systems, Commercial Operators and LEO Constellations Drive Rapid Expansion

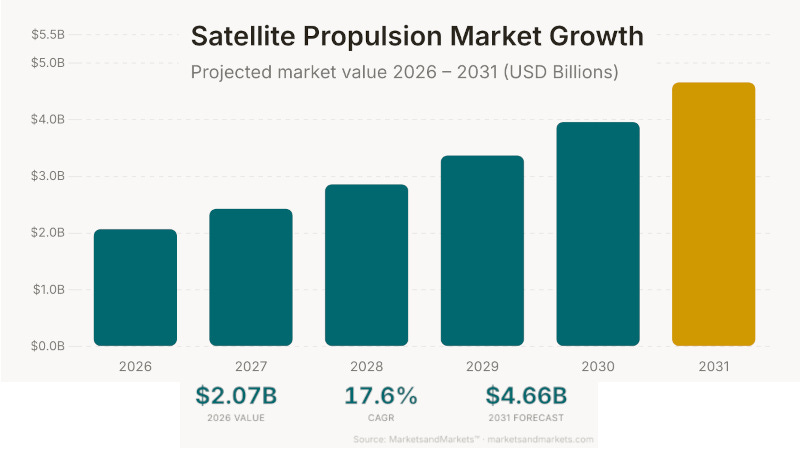

The global satellite propulsion market is forecast to more than double in size over the next five years, growing from $2.07 billion in 2026 to $4.66 billion by 2031, a compound annual growth rate of 17.6%, according to a new market analysis from MarketsandMarkets. The expansion reflects a fundamental shift in how satellites are designed, launched and operated across an increasingly complex and competitive orbital environment.

Demand is being fueled by broader and more ambitious use of satellites across communications, earth observation, navigation and defense. As operators expand constellations and put higher-value spacecraft into orbit, propulsion systems have moved from secondary consideration to mission-critical hardware — needed not just at launch, but continuously throughout a satellite’s operational life for station keeping, collision avoidance, repositioning and controlled deorbiting at end of service. The result is increasing pressure on satellite manufacturers and their propulsion suppliers to deliver systems that are lighter, more fuel-efficient and capable of supporting longer missions without driving up launch costs.

By propulsion technology, the electric segment is expected to post the highest growth rate, recording a CAGR of 18.1% through 2031. Electric propulsion offers a compelling tradeoff for satellite operators: lower propellant mass compared to chemical systems, greater fuel efficiency and longer operational endurance. Those advantages have made it the default technology for many large-scale constellation operators managing hundreds of spacecraft and facing tight per-unit cost constraints. Continued development of miniaturized electric thrusters and power-efficient designs is expected to accelerate adoption across satellite classes.

The commercial sector is expected to account for the largest share of the propulsion market throughout the forecast period. Private operators are launching at an accelerating pace for broadband internet, communications, earth observation and Internet of Things applications. The rise of large LEO constellations — some numbering in the hundreds or thousands of satellites — has created sustained, high-volume demand for propulsion systems that are both affordable and reliable. Each satellite in such a constellation requires propulsion for orbit raising, active station keeping, collision avoidance maneuvers, repositioning and, increasingly, a controlled re-entry to avoid contributing to orbital debris. That operational profile makes propulsion a recurring cost driver across a constellation’s full lifecycle.

By platform weight class, the medium satellite category ... spacecraft between approximately 2,648 and 4,409 pounds (1,201–2,000 kg) ... is projected to be the fastest-growing segment during the forecast period. These satellites typically carry heavier payloads, operate on mission timelines measured in years and require more capable propulsion than smaller spacecraft. Electric propulsion is increasingly favored for this class, delivering the performance needed for complex missions while keeping overall satellite mass within launch vehicle constraints and reducing long-term fuel costs.

Geographically, the United States is estimated to hold an 84.6% share of the global satellite propulsion market in 2026, reflecting the country’s dominant position in commercial satellite manufacturing, launch services and government space programs. Among growing regions, Asia Pacific is projected to be the second-fastest-growing market, driven by national investment programs in China, India, Japan and South Korea spanning commercial communications, defense surveillance and weather monitoring.