Satellite Ground Station Market Projected to Triple in Value by 2035

Allied Market Research Report Forecasts $230.9 Billion Market, Driven by LEO Expansion and IoT Demand

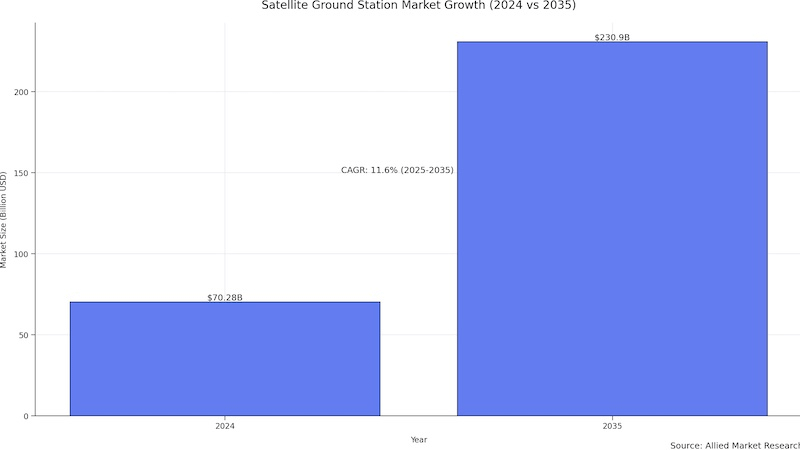

The global satellite ground station market is on track to more than triple in value over the next decade, reaching $230.9 billion by 2035 from $70.28 billion in 2024, according to a new report published by Allied Market Research. The forecast represents a compound annual growth rate of 11.6% from 2025 to 2035.

The market encompasses terrestrial facilities equipped with antennas, radio frequency systems, transmitters, receivers, modems, and network management infrastructure that enable communication with orbiting satellites. Ground stations perform telemetry, tracking, and command operations, along with data uplink and downlink, signal processing, and network integration for applications ranging from broadband communications and earth observation to navigation, weather monitoring, defense surveillance, and space research.

Driving Growth

The rapid scale-up of low Earth orbit satellite constellations is cited as a primary demand driver. LEO operators including SpaceX’s Starlink and Amazon’s Project Kuiper are accelerating deployment of automated, cloud-integrated ground station networks to support continuous connectivity and low-latency services. The expansion of satellite-based IoT connectivity is generating additional demand, as industries deploy connected devices in remote regions where terrestrial networks are unavailable. Sectors including agriculture, mining, oil and gas, maritime, logistics, and environmental monitoring are relying on satellite IoT for real-time asset tracking, predictive maintenance, and remote operations.

The report identifies rising demand for satellite communication services in both developed and emerging markets as a key growth catalyst. In India, demand is being fueled by national initiatives for digital inclusion, rural broadband connectivity, smart infrastructure, and resilient networks for disaster response. The Indian Space Research Organisation is expanding satellite communication capacity while NewSpace India Limited is commercializing space services, strengthening India’s domestic ground station ecosystem. Increased private sector participation, supported by policy reforms and growing investment, is also boosting deployment of new ground stations and upgrades of existing facilities across the country.

High capital investment remains a significant constraint on market expansion. Establishing a ground station requires substantial upfront expenditure on land, site development, antenna systems, radio frequency equipment, tracking and telemetry hardware, control software, cybersecurity systems, and high-reliability power and cooling infrastructure. Recurring operational and maintenance costs, including the need for skilled technical personnel and continuous technology upgrades to remain compatible with new satellite constellations and evolving communication standards, add further financial burden. The rapid technology refresh cycles driven by LEO constellation deployments make it difficult for smaller operators and emerging-market players to scale profitably.

Market Segments

The report segments the market by platform, function, orbit, end user, and region.

By platform, fixed ground stations held the largest market share in 2024. Mobile stations are projected to grow at the fastest rate during the forecast period.

By function, communications applications dominated the market in 2024. The navigation segment is anticipated to record the fastest growth rate.

By orbit type, LEO segments led the market in 2024. GEO-supporting infrastructure is projected to grow at the fastest rate going forward.

By end user, commercial operators accounted for the largest share in 2024. Defense applications are anticipated to grow at the fastest rate during the forecast period.

Regional Outlook

North America held the largest regional share of the satellite ground station market in 2024, supported by strong government funding, established commercial and defense space operators, and advanced technological capabilities. NASA, the U.S. Space Force, and a robust ecosystem of private space companies anchor the regional market. Growing demand for secure defense communications, high adoption of cloud-based ground station services, and increasing investment in space situational awareness and deep space missions support continued dominance.

Europe ranks as the second-largest regional market, supported by coordinated space programs through the European Space Agency and national space agencies. Germany, the United Kingdom, and France are key contributors, with well-established satellite communication networks and ground infrastructure supporting defense, broadcasting, and environmental monitoring applications.

Asia-Pacific is the fastest-growing region in the market. China, India, Japan, and South Korea are significantly expanding their ground station networks to support domestic satellite constellations and deep space missions. ISRO continues to strengthen India’s ground segment capabilities across navigation, communication, and planetary exploration, while broadband demand in remote areas and government-led space commercialization initiatives accelerate regional investment.

The full report — “Satellite Ground Station Market by Platform, Function, Orbit, and End User: Global Opportunity Analysis and Industry Forecast, 2025-2035” — is available from Allied Market Research.