Satellite and Spacecraft Subsystem Industry Report 2023-2033

Market Has Experienced Remarkable Growth, According to BIS Research

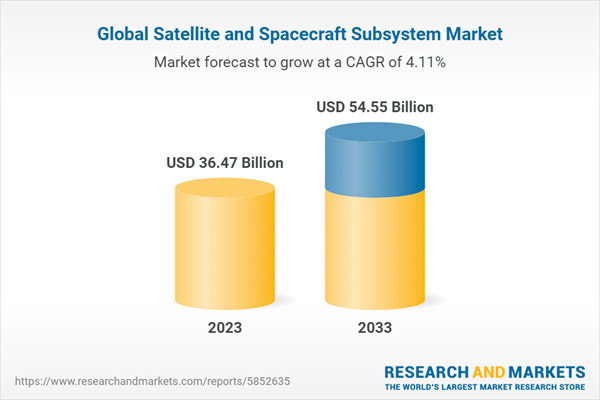

The global satellite and spacecraft subsystem market is projected reach a value of $54.55 billion by 2033, up from $36.47 billion in 2023, growing at a CAGR of 4.11%

According to a recent report from BIS Research, the global satellite and spacecraft subsystem market has experienced remarkable growth in recent years due to the increasing advancements in technology and the emergence of new applications. This growth is primarily driven by the commercial space industry, which has demonstrated its continuous expansion and robust growth, with record-breaking numbers of satellite launches and a significant increase in the overall number of active satellites in orbit.

The development of SmallSats and CubeSats has attracted the interest of private companies and government agencies by offering more affordable access to space and enabling new business models, such as satellite constellations. SmallSats, which accounted for approximately 95% of satellites launched in 2022, have played a significant role in expanding the industry's capabilities.

This continuous coverage is particularly valuable for applications such as telecommunications, Earth observation, and positioning systems, where uninterrupted connectivity and data acquisition are essential. The availability of satellite constellations opens new possibilities for a wide range of industries, including telecommunications, agriculture, climate monitoring, disaster response, and more.

According to the report, in 2022, 2,243 commercial satellites were successfully deployed into orbit, marking a remarkable increase of over 32 percent compared to 2021. Additionally, the market is driven by the rising adoption of the increasing demand for artificial intelligence in space. By leveraging AI in satellite and spacecraft subsystems testing and deployment, engineers and operators can enhance performance, improve reliability, and optimize operational efficiency.

The utilization of AI technologies can lead to more advanced and capable subsystems, enabling the successful execution of missions and the realization of the full potential of satellite and spacecraft operations. Notable companies include Airbus S.A.S., Lockheed Martin Corporation, Northrup Grumman, Date Device Corporation, and among others. These companies heavily invest in research and development to introduce innovative and advanced subsystems.

Furthermore, satellite constellations are expected to drive the space market during the forecast period. These constellations provide global or near-global coverage, ensuring that at least one satellite is available at any time and location on Earth.

Industrial Impacts

Increased investment from private industry has emerged as a significant driver of growth in the global satellite and spacecraft subsystem market.

This surge in private sector investments has fostered heightened competition, innovation, and the emergence of new business models, such as mega constellations comprising hundreds or thousands of satellites in low Earth orbit (LEO) to deliver services such as low-latency broadband.

It is anticipated that by the end of 2023, over 5,000 broadband satellites will be in LEO, providing high-speed internet to millions of subscribers across the globe. Private companies such as SpaceX, Blue Origin, and Relativity Space are actively investing in the development and commercialization of innovative technologies such as reusable launch vehicles.

Market Segmentation

Commercial Segment dominates the Global Satellite and Spacecraft Subsystem Market (by End User)

The global satellite and spacecraft subsystem market was led by the commercial end user, generated $27,778.0 million in 2022, and is expected to reach $43,686.6 million in 2033 at a CAGR of 3.61% during the forecast period 2023-2033. The demand for satellite communication services is surging in the commercial sector.

Companies require reliable and efficient communication systems for a wide range of applications, including broadband internet services, telecommunication networks, and data transfer. These services heavily rely on satellite and spacecraft subsystems for signal transmission, data processing, and reception.

Furthermore, the trend toward small satellites, including CubeSats and nanosatellites, is particularly prominent in the commercial space sector. These smaller satellites offer cost-effectiveness and rapid deployment opportunities for various applications.

Payload Segment Leads the Global Satellite and Spacecraft Subsystem Market (by Satellite Subsystem)

The global satellite and spacecraft subsystem (satellite subsystem) market is expected to be dominated by the payload in 2023.

Payloads are critical components of satellites that carry instruments and equipment used to collect and process data for various applications. As the demand for satellite-based data and services continues to grow across sectors such as communication, Earth observation, weather monitoring, navigation, and scientific research, the need for advanced and specialized payloads increases.

Additionally, as governments, businesses, and research institutions increasingly rely on satellite data for decision-making, the demand for such payloads rises significantly.

North America is anticipated to grow at a CAGR of 3.02%

The presence of a larger number of established satellite and spacecraft subsystem providers is driving the market in the region. The presence of major industry players such as Northrop Grumman, Teledyne Technologies, Texas Instrument, Data Device Corporation, and Microchip Technology Inc. within the region with growth strategies such as partnerships are paving the way for market opportunities.

Additionally, the strategic adoption of 3D printing technology by the U.S. companies in this sector is a deliberate choice. By leveraging 3D printing, these companies can reduce satellite and spacecraft complexity while enhancing the overall manufacturability of satellite and spacecraft subsystems.

The U.S. dominates the global satellite and spacecraft subsystem market in the region, with various key players dedicated to developing rockets that are specifically designed to meet the requirements of commercial enterprises and government organizations involved in launching payloads into low Earth orbit (LEO), medium Earth orbit (MEO), geostationary equatorial orbit (GEO), and beyond.