LEO Satellite Market worth $23.2 Billion by 2029

Driven by the Growing Need for Earth Observation Imagery and Analytics

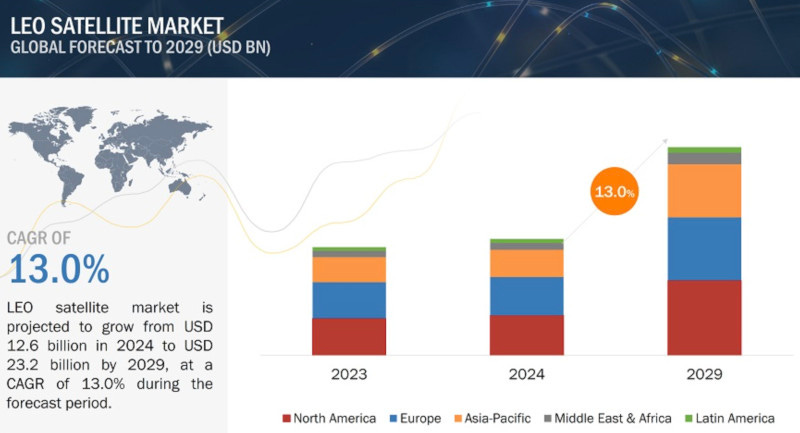

The LEO satellite market is projected to grow from $12.6 billion in 2024 to $23.2 billion by 2029, at a CAGR of 13.0% from 2024 to 2029 according to a new report by MarketsandMarkets. The market growth can be attributed to the growing need for earth observation imagery and analytics.

The LEO satellite market holds a huge potential for data service providers, satellite service providers, remote sensing service providers, technical service providers, and investors. Versatility, low cost, advanced mechanics, ease of assembly and launch, mass production, and short life cycles have driven investments in LEO satellites. The amount of satellite data and range of applications for data will continue to grow in the future as new technologies develop and more satellites become operational.

The adoption of off-the-shelf CubeSats and reusable rocket technology is also expected to fuel market growth. The market is growing due to the demand for higher bandwidth internet. If the current satellite internet proposals become a reality, as many as 50,000 satellites will be orbiting in LEO within 10 years. However, space debris caused by LEO satellites and some regulatory challenges are expected to hinder market growth.

The LEO satellite market report includes small satellites (1–500 kg or 2.2 - 1,100 pounds), medium satellites (500–1,000 kg or 1.100 - 2,200 pounds), and large satellites (more than 1,000 kg or 2,200 pounds). These satellites are used for communication, earth observation & remote sensing, mapping & navigation, scientific research & exploration, surveillance & security, space observation, and various other applications by defense, intelligence, civil, commercial, and government users. The continuous miniaturization of satellites through technological advancements in electronics, low mission costs, and increasing use of satellite constellations (containerization) are major drivers for the growth of this market. LEO satellites are also considered disruptive technology by several space organizations.

In terms of satellite mass, the LEO satellite market is divided into four main categories: small satellites, medium satellites, CubeSats, and large satellites. Small satellites are replacing large-sized satellites by becoming capable of performing in a vast range of commercial applications. Advancements in the miniaturization technologies and applications of satellite constellations are the key factors driving the adoption of small satellites. The minisatellite, a sub-type of small satellite, is described as an LEO satellite having a wet mass (including fuel) of 101 kg to 500 kg (222 - 1,100 pounds). Minisatellites are present at an altitude of about 1,000–5,000 km (≈620 - 3,100 miles). The operational cost, as well as the manufacturing cost of minisatellites, is less than that of traditional larger satellites, thereby offering a low-cost solution to gather and communicate data. Advancements in miniature electronics components reduce the cost and provide enhanced capabilities for commercial and defense usage.

The LEO satellite industry is categorized by application into communication, earth observation & remote sensing, scientific research, and technology, and others. A communication satellite is responsible for creating a communication channel to receive signals for telephone, television, internet, and military communication. The demand for communication satellites is growing due to the ever-increasing demand for high-speed satellite internet and precise information in the military communication chain of command. Moreover, Advancements in technologies have helped overcome major hurdles faced in providing efficient miniaturized onboard power systems for advanced communication hardware on satellites that require high electrical power. This has been useful for generating higher data rates, thereby improving the overall communication capabilities of nanosatellites, microsatellites, and minisatellites. LEO satellites can accommodate more sophisticated payloads than traditional larger satellites. They also take considerably less time to transfer the data from the Earth to LEO due to the closer location of satellites from the earth than GEO, where the traditional large satellites are located. LEO satellites enhance communication capabilities such as disaster management, asset tracking, and mobile communication.

The Asia Pacific market is projected to witness a significant CAGR from 2024 to 2029. The Asia Pacific Regional Space Agency Forum (APRSAF) enhances space activities through human resource development, capacity building, and development of science-technology capability in the region. Space agencies, governmental bodies, international organizations, private companies, universities, and research institutes from over 40 countries and regions take part in APRSAF, the largest space-related conference held annually in the Asia Pacific region, leading to various growth strategies, technological advancements, research and development activities, innovation in small and CubeSats, and development of reusable launch vehicles in terms of design, function, and integration.

The major players in LEO satellite companies include SpaceX (US), Airbus Defence and Space (Germany), Lockheed Martin Corporation (US), Northrop Grumman Corporation (US), and L3Harris Technologies, Inc. (US).