LEO Satellite Market Worth $20.69 Billion by 2030: Report

Rapid Growth Largely Fueled by the Increasing Demand Across Multiple Verticals

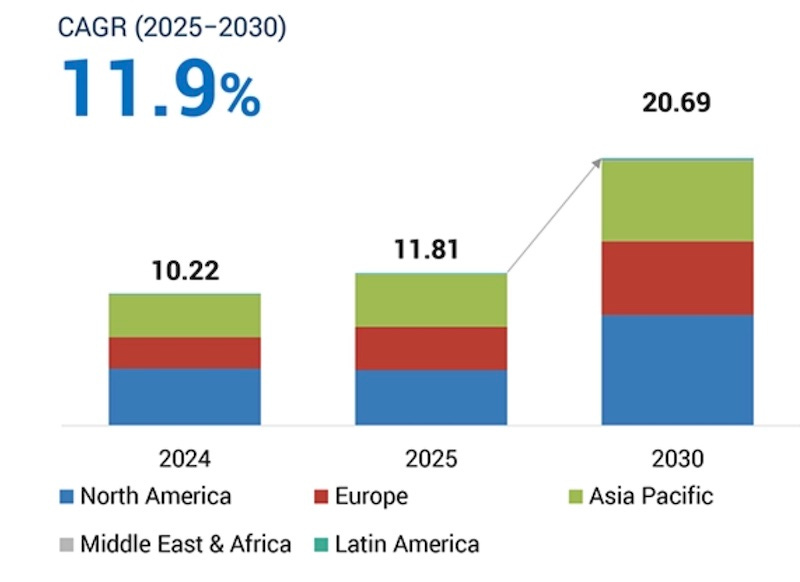

The LEO satellite market is projected to grow from $11.81 billion in 2025 to $20.69 billion by 2030, registering a CAGR of 11.9% according to a new report from MarketsandMarkets. The market for LEO satellites is experiencing rapid growth, largely fueled by the increasing demand for high-resolution Earth observation, real-time analytics, and global broadband connectivity. Other factors driving the market include advancements in miniaturized satellite technology, reduced launch costs due to reusable rockets like SPACEX's Falcon 9, and the extensive use of off-the-shelf CubeSats for commercial missions.

These developments have made it easier for private companies and start-ups to enter the market. Future growth is anticipated to be bolstered by new satellite constellations aimed at achieving global internet access. Projects like Amazon's Kuiper and OneWeb plan to deploy tens of thousands of satellites. However, challenges remain. The most pressing issues include the risks of orbital congestion and space debris, which have raised regulatory concerns among international space agencies. The management of the radio frequency spectrum and the coordination of global satellite traffic also continue to pose technical and policy challenges.

The LEO satellite market is categorized into four types based on satellite mass: small satellites, medium satellites, CubeSats, and large satellites. Small satellites are increasingly replacing larger satellites due to their ability to perform a wide variety of commercial applications. Key factors driving the adoption of small satellites include advancements in miniaturization technologies and the use of satellite constellations. A specific type of small satellite is the minisatellite, defined as a LEO satellite with a wet mass (including fuel) of 101 to 500 kg (≈222-1,100 pounds). Minisatellites typically operate at altitudes between 1,000 and 5,000 km (≈621-3,100 miles).

The market is divided by application into communication, earth observation & remote sensing, scientific research, technology, and other applications. Communication satellites create channels to receive signals for telephone, television, internet, and military communications. The demand for these satellites is increasing due to the need for high-speed satellite internet and accurate information in military communication networks. Advancements in technology have helped address significant challenges in providing efficient miniaturized onboard power systems for advanced communication hardware on satellites that require substantial electrical power.

North America is home to leading satellite manufacturers and launch service providers, as well as technological innovators like SPACEX, OneWeb, and Northrop Grumman, who are actively expanding broadband connectivity and advanced data services to emerging markets. Government agencies such as NASA, the Department of Defense, and the Federal Communications Commission (FCC) fuel industry growth by funding relevant research, establishing favorable policies and regulations for developing specialized satellites, and facilitating spectrum allocation. The region also benefits from strategic private investments and public-private partnerships that drive innovation and enhance satellite design, manufacturing, and launch operations.

Key players in the LEO satellite companies include SPACEX (US), which leads with its Starlink broadband constellation; Airbus Defence and Space (Germany), known for building advanced Earth observation and communication satellites; and Lockheed Martin Corporation (US), which provides integrated satellite platforms for military and civil missions.

Other players in this market include Thales Alenia Space (France), OneWeb (UK), Surrey Satellite Technology Ltd. (SSTL) (UK), Planet Labs PBC (US), Sierra Nevada Corporation (US), Maxar Technologies (US), GomSpace (Denmark), Mitsubishi Electric Corporation (Japan), Exolaunch GmbH (Germany), China Aerospace Science and Technology Corporation (CASC) (China), BAE Systems (UK), RTX Corporation (US), OHB SE (Germany), The Aerospace Corporation (US), Millennium Space Systems (US), and Kuiper Systems LLC (US).