CLPS at 30 The Revenue Math Behind NASA’s Lunar Landing Acceleration

What the 30-landing target actually signals for Intuitive Machines, Firefly Aerospace, Astrobotic, and the commercial lunar payload economy

WHAT THIS MEANS

NASA’s Ignition announcement targeting up to 30 CLPS robotic lunar landings starting in 2027 is a real and sustained demand signal — but the revenue math is structurally constrained in ways the headline count obscures. At an average task order value of approximately $180M and a payload capacity ceiling that no current lander meets at Phase 1 scale, the program requires a new CLPS 2.0 contracting vehicle that does not yet exist. The commercial payload market remains supplemental to NASA-funded revenue for every active provider. Investors and C-suite leaders who treat ‘30 landings’ as uniformly bullish for all CLPS providers are misreading the signal: the provider best insulated from structural constraints is the one with a $4.82B government communications contract backstopping its balance sheet — not just a CLPS task order count.

And Why the Headline Number Misleads

Four metric tons. Seven payloads. $180.4 million.

Those three numbers are the actual content of NASA’s most significant commercial lunar signal in years, and they have very little to do with the headline figure that spread across every space trade outlet on March 23, 2026. NASA’s Ignition initiative announced a target of up to 30 robotic lunar landings starting in 2027 under its Commercial Lunar Payload Services program. The 30 figure is real. It is also, for investors trying to model company-level revenue, the least useful number in the announcement.

The useful numbers are the ones that determine whether Intuitive Machines, Firefly Aerospace, Astrobotic Technology, and a new wave of CLPS 2.0 entrants can build financially sustainable businesses at the new cadence. This article runs those numbers. The picture is more nuanced than the headline, and the answer is different for each provider.

What the IDIQ Actually Allows

Before mapping the revenue, it helps to understand the legal container that holds it. The CLPS program operates under an indefinite delivery, indefinite quantity contract with 14 eligible vendors and a ceiling value of $2.6 billion, running through November 2028. As of February 2024, NASA had awarded eight task orders valued at a combined $984.3 million after accounting for cost growth. That cost growth averaged 26 percent across the program. Average schedule slippage ran to 14 months per task order. Those figures come from a NASA Office of Inspector General audit published in June 2024, and they are the most important contextual facts in the CLPS investment thesis that almost nobody includes in their buy-side analysis.

Now run the 30-landing math against the IDIQ ceiling. If average task order values continue on their current trajectory, a reasonable midpoint estimate is $150 million per mission. Thirty missions at $150 million is $4.5 billion. The current CLPS 1.0 IDIQ ceiling is $2.6 billion. Those two numbers do not coexist. The 30-landing Ignition target is structurally dependent on CLPS 2.0, a new contracting vehicle NASA committed to establishing by the end of Fiscal Year 2026. If CLPS 2.0 is delayed, the legal authority to fund 30 missions at anything near current task order values does not exist. That is not a bear case. It is the baseline legal reality.

The contract value trajectory itself tells a secondary story worth noting. Astrobotic’s first Peregrine task order, awarded in May 2019, came in at $79.5 million for 14 NASA payloads. Firefly’s Blue Ghost Mission 1, awarded in 2021, came in at $93.3 million for 10 NASA payloads. Intuitive Machines’ IM-5, awarded March 23, 2026, came in at $180.4 million for seven NASA payloads. The payload count per mission has declined as the task order value has grown — a pattern that reflects how NASA thinks about mission complexity and payload integration maturity over time.

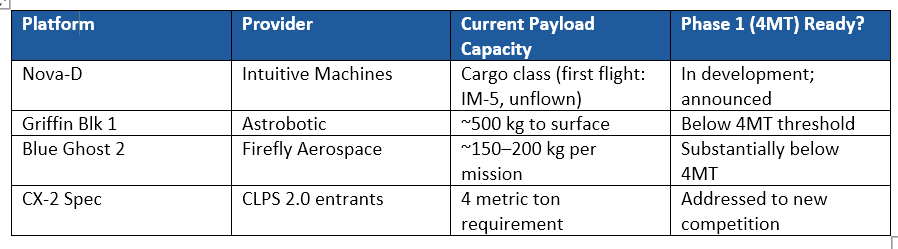

The Lander Capacity Table

NASA’s Ignition fact sheet specifies that Phase 1 CLPS landers should carry up to four metric tons of payload per mission. That specification matters for investors because not one active CLPS lander operates at that capacity today.

The gap between current platform capacity and the Phase 1 4MT specification is not a flaw in NASA’s planning. It is the program structure. Phase 1 is explicitly framed as ‘Build, Test, Learn,’ with the 30-landing cadence serving as the operational baseline for technology maturation before crewed surface operations. What it does mean for investors is that the ‘30 landings at Phase 1 scale’ headline blends two distinct periods: a near-term period using current platforms in the sub-500 kg range, and a medium-term period requiring new or significantly upgraded landers procured under CLPS 2.0. Treating 30 as a uniform demand signal across that entire arc overstates near-term revenue capacity per mission.